Energy: When will it finally get some investor love?

The more hated it gets, the more compelling it becomes as a hedge should the technology driven bull market unravel. Oil and gas are still serving an important function for the economy.

Disclaimer: The information contained in this article is not and should not be construed as investment advice. This is my investing journey and I simply share what I do and why I do that for educational and entertainment purposes.

TLDR Summary

Institutions underweight it. Retail dumps it. Derivatives traders short it. Energy is by far the most hated sector out there which sets it up nicely for a squeeze should the right spark occur. Fund managers are more underweight today than they were at the peak of the pandemic. And that preceded 50% sector outperformance in 2022.

In a bull market driven by software and semiconductors, energy is a risk-off sector. You bet on it when you want to bet against productivity gains in the darling industries. Energy doesn’t participate in the hottest innovation themes of our times. It’s a hedge against their failure. Investors pay for that insurance through an inferior return during good times. But the more hate energy gets, the more overextended the bull market in other segments likely is and the more attractive the hedge becomes.

The curious thing about energy is that it is quietly riding its own innovation cycle. The US oil production boom has created tremendous value by cutting energy costs for consumers and businesses which has fueled economic growth. The US economy has been bailed out by fracking engineers and the world is asleep on it. At some point, those creating that value should also capture some of it, no?

Browsing through the last five years of sector performance and sentiment

Energy was one of the most punished sectors in 2020. First, the economic standstill from lockdowns crushed demand. Then, the energy transition took off as an investment theme. People wanted to bet on solar, batteries and lithium rather than oil and gas.

This changed rapidly in 2021. The economy recovered from lockdowns and as it turned out, it was still running on fossil fuels. The greatest inflation surge in more than 40 years provided a lift for all commodities and Russia’s Ukraine invasion in 2022 put the cherry on top of the icing of the energy cake.

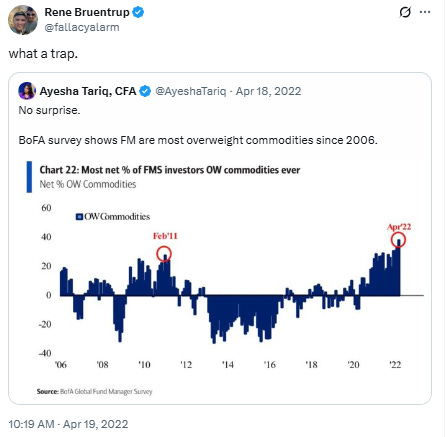

By April of that year, institutional investors were the most overweight commodities since 2006. And that had been shortly before the GFC popped one of the greatest commodity bubbles ever.

As happens so often, investors trapped themselves because they mistook cyclical forces for structural ones. It took a while for that to sink in. The entire year 2022 was full with energy bull porn. Prominent macro and industry analysts like Lyn Alden argued that energy prices have entered a long term bull run after years of underinvestment due to misguided ESG considerations. Oil and gas would be needed for a very long time until alternative energy sources can replace them at scale, if they ever can. And even then, hydrocarbons would still be required for petrochemical purposes.

These arguments had merit from a theoretical perspective as usually is the case when investors and analysts are trying to justify price action. What they missed was that asset prices had already priced all of that in and more. Too many people were in the trade which is why it had to fail. I laid that out in the article below.

And sure enough, XLE 0.00%↑ (the most popular sector ETF) underperformed SPY 0.00%↑ by 26% in 2023. The oil price had started that year at $80 and ended it at $70. Many energy bulls got crushed and this made me curious about whether the sector was becoming attractive again.

I did indeed find enough bullish arguments to get somewhat excited and summarized them in the article below.

It seemed that there was enough capitulation among bulls, evident in institutional investor positioning and derivatives positioning. Energy positioning had gotten quite low among institutional investors. Shortages had become excess supply. Sanctions were ineffective in curbing supply. Hydrocarbons just found alternative ways around the globe.

Given that capitulation, I felt that the sound fundamental arguments could make the investment shine again. After all, fossil fuels are still and will continue to be important for economic growth, which would likely surprise to the upside given irrational recession fears at that time. Oil and gas companies were financially sound with strong balance sheets. And I also felt that the sector would benefit from Trump’s potential second term.

While my original bear case on oil and gas aged well, I can’t say the same so far for the bull case published a year later. XLE has underperformed the S&P 500 by another 24% since January 2024. And that happened in spite of a continued robust US economy, growing energy demand from the AI boom and Trump’s victory.

The longer the sector underperforms and the more hated it becomes, the more I am wondering whether I was wrong or just too early. Time to take another look.