Here's a parallel between 2008 and today.

You're not going to like this analogy. But I'll tell you anyway.

Disclaimer: The information contained in this article is not and should not be construed as investment advice. This is my investing journey and I simply share what I do and why I do that for educational and entertainment purposes.

This article is entirely free to read.

TLDR Summary

A foundational law in investing is the congruence between return and risk. The more return you want, the more risk you have to bear. Since the beginning of investing, people have tried to cheat this law by finding ways to earn more than the risk they are willing to bear would justify. Usually leverage was employed as a key ingredient. Sooner or later these attempts have failed in every instance.

The 2008 subprime crash is a famous example. Financial alchemists thought they had found a magic formula to make risk vanish through diversification. A false sense of safety made investors lever up too much. And then they got wiped out when it all failed. After all, risk redistribution did not mean risk cancellation.

Today’s equivalent of that is Bitcoin which is deemed the jack-of-all-trades. Superior returns AND superior hedging function against menaces like inflation, recession and turmoil in general. It promises the returns of a Nasdaq sweetheart without the operating risks.

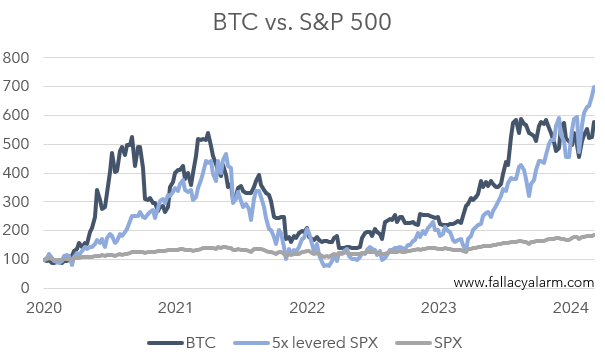

How many investors understand that their Bitcoin holding is a five times leveraged S&P 500 bet in disguise? In a risk-off moment, they will be on the hook just like everyone else.

The total leverage in the Bitcoin economy is unknown just like the total subprime leverage was unknown. The MicroStrategy microcosm provides clues how insane it is. But there is no data on implicit leverage. What I mean by that is that we don’t know what investors would own if there was no Bitcoin. If the answer was stocks, we might be fine. But if the answer is cash, people might be owning much more risk assets than they would own in other circumstances.

A speculative attack on explicit and implicit leverage in the Bitcoin community is only a question of time. And it has reached a size that makes contagion likely in that case. The next 50% drawdown in Bitcoin will likely not be caused by the next 10% S&P 500 correction. It will likely be the driver for it.

What happened back then?

A famous example where an attempted cheat of the return risk congruence failed is the crash of subprime mortgages in 2007/08 that launched the Global Financial Crisis and later the Great Recession. Much has been said about this matter. But a quick recap helps as context for the point I am making further below.

Leading up to the GFC, the US private sector had a lot appetite for credit (which was interestingly in part driven by a lack of fiscal deficits that would have provided them with savings to avoid borrowing).

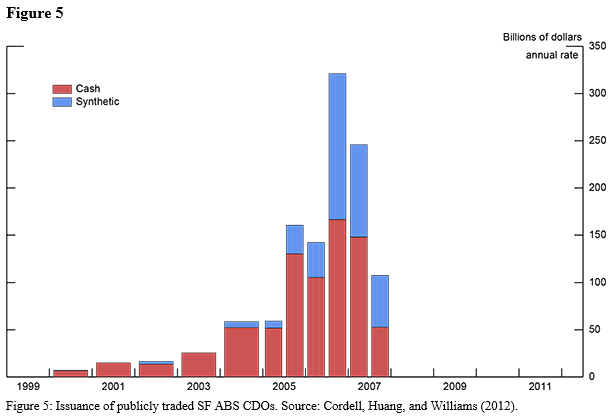

The financial sector provided the capital for this demand through securitization. Mortgages (that account for about 70% of household borrowings) were put into pools called collateralized debt obligations (CDOs) which had various tranches ranked by the seniority of claims.

These CDOs promised risk mitigation through diversification. Investors got (or at least believed they got) securities with the risk of a AAA-rated security that earned them returns much higher than most AAA-rated securities. It was a magical example of financial alchemy that seemingly removed risk from the system to make everyone earn more.

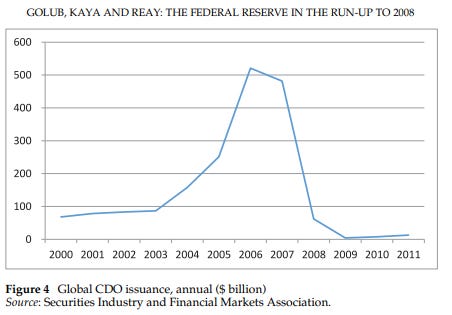

Due to their attractive risk/return-profile, these CDOs were highly sought after. The global annual issuance swelled from less than $100bn in 2003 to more than $500bn by 2006.

For reference, the US Treasury - the main provider of fixed income securities - supplied less than that during those years.

Demand for these investment products was so huge that banks came up with synthetic structures to artificially increase their supply.

For example, they issued credit default swaps (CDS) to willing speculators. These CDS were insurance policies on their underlyings. If they defaulted, the CDS would pay the difference. The cost of a CDS was typically the yield difference between the underlying and a AAA-rated government bond. Therefore, the banks could create synthetic mortgage-based CDOs by pooling government bonds with a short position in the CDS. Think of this like the equivalent of an equity portfolio where you buy the S&P 500 and sell TSLA 0.00%↑ puts against it naked.

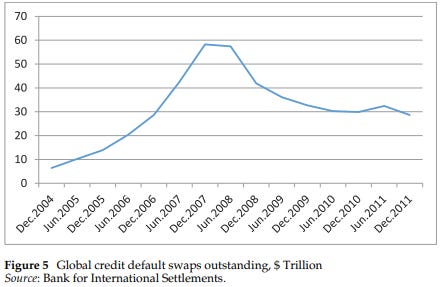

The global CDS market ballooned from less than $10tn in 2004 to almost $60tn in 2007. It should be obvious that much of this was more than just insurance. It was hidden leverage in the system.

By 2006, synthetic CDOs accounted for a substantial share of the overall CDO issuance.

Ultimately it failed as we all know. The risk wasn't gone just because it was redistributed. Investors took too much risk and got wiped out.

What is an equivalent of that today?

Bitcoin. It promises equity-like returns without bearing equity-like risk (broadly defined as operating risk as opposed to narrowly defined as volatility). It’s deemed to be the jack-of-all-trades among the available assets out there. Superior return AND superior hedging function.

People buy it as a hedge against inflation and market turmoil. They do understand that it comes with increased volatility. But do they understand how closely it correlates with the S&P 500? Do they understand the $2tn Bitcoin market cap trades like a $10tn investment into the S&P 500?

Bitcoin is not a hedge against chaos like Gold for example. When the world ended in 2020, Bitcoin tanked alongside stocks while Gold pumped. During the stimulus driven pandemic bull market, Bitcoin pumped with stocks while Gold consolidated.

Bitcoin is not a risk-off asset. It’s a risk-on asset on steroids. And not even a very good one. What will happen when people realize Bitcoin won’t make them participate in the innovation themes and productivity gains in the future? Will they still pour into it?

And if it ever became a risk-off asset, it would pay for that insurance function with a lower return vs. stocks. Gold has appreciated by 5% annually for the last 100 years. The total return of the S&P 500 over the same period is 10.6% annually. That’s the price to insure against WWIII.

Where does Bitcoin come from?

To understand the nature of Bitcoin, it’s helpful to think for a moment how it was born and how it gained traction. It was invented under the impression of two massive crashes in 2000 and 2008 that shook investor confidence in productive assets as a store of value.

Crashes like this had not happened since 1929. Even WWII was better for US investors than 2000-2009. And then the pandemic hit with a blitzcrash of similar magnitude. Followed by the worst inflation shock in decades the aftermath of which made many popular stocks drop 90%+. The last 25 years have been quite brutal if you think about it.

All of that left scars in investor minds. Fears about recessions and inflation wiping out corporate profits are engraved into our zeitgeist. Accelerating business cycles and innovation cycles aren't helping either. Entire industries go from just fine to doom and gloom in just a few years. Think about automotive, (office) real estate or airlines.

That's the necessary context to understand today's affection for Bitcoin. It's not a productive asset. It can't fail doing something because it is not designed to do anything.

This provides investors with a (false) sense of safety. As a result they lever up and take too much risk. Look at the MicroStrategy MSTR 0.00%↑ microcosm with various layers of leverage on top of each other. Owners of leveraged ETFs like MSTX 0.00%↑ and MSTU 0.00%↑ are playing macro with 20x leverage.

These two ETFs control $5bn of MicroStrategy shares. The entire company was worth less than that just two years ago!

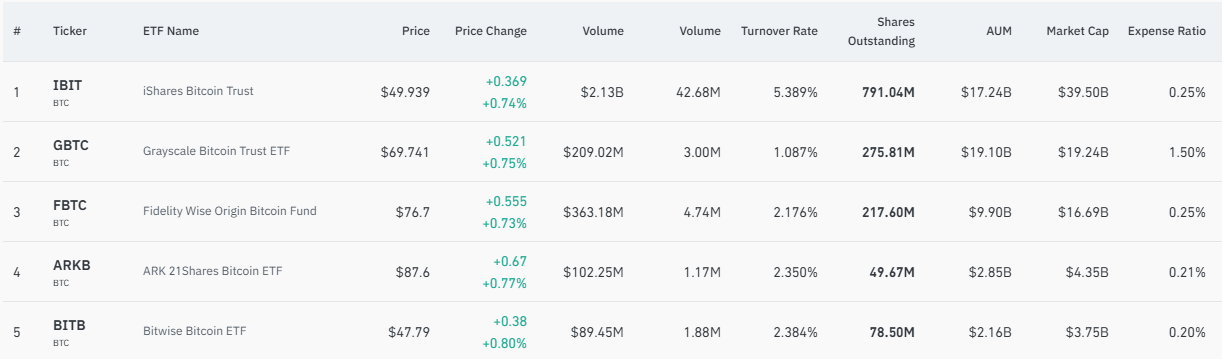

Or look at the insane demand for spot ETFs launched earlier this year such as IBIT 0.00%↑ or FBTC 0.00%↑, possibly the most successful ETF launches in history. The five largest spot ETFs have accumulated $85bn (!) in the first 10 months of their existence.

Allegedly, 40% of Americans own crypto today. It rivals the adoption of stocks, especially for younger generations. It’s a mania that I find very hard to comprehend.

The entire leverage in the Bitcoin economy is unknown because we don't know what investors would own instead if there was no Bitcoin. Would they own stocks instead? Or cash? If the answer is the latter, then this is implicit leverage because people own more risk assets than they would own in other circumstances. It's only a question of time that the leverage in the Bitcoin economy will be tested through a speculative attack on weak and overleveraged hands.

Sincerely,

Your Fallacy Alarm

“Bitcoin is not a risk-off asset. It’s a risk-on asset on steroids. And not even a very good one.”

Strong.

Great article 🙌

interesting but wrong