KRE: Banking on the Pivot

Bleak sentiment and unambitious valuation despite operating resilience.

Autopilot to Anguish?

Monetary policymakers seem to be completely out of control with the steepest hiking cycle ever. They seem to be determined to keep interest rates high, defying the reality that inflation has been a non-issue for pretty much 6 months. They are running the US banking system into the ground. If they continue to do so, many banks will lose their livelihood as their asset portfolios are impaired and the yield curve inversion will make it eventually impossible to earn a positive interest margin.

But: Betting on this inevitable fiasco would be too easy in my opinion. Humans have the remarkable ability to find the right solution after exhausting all alternatives. If something is obviously unsustainable, it will be reversed. And sometimes this happens faster than can be reasonably anticipated. Economic and financial data points are writing it on the wall already. We will likely see short-term yields come down hard over the coming 12 months.

In this article I will outline why I believe US regional bank stocks are attractive vehicles to bet on this pivot. This belief is based on three pillars:

Bleak sentiment and unambitious valuation levels

Remarkable financial resilience from an aggregate perspective

Strong underlying business fundamentals

What is KRE?

KRE 0.00%↑ is an ETF targeting to replicate the performance of the S&P Regional Banks Select Industry Index. It comprises 144 financial institutions in the US with a combined market cap of ~$400bn. They are home to $3.3tn in customer deposits, which represents approximately 20% of the US banking sector. The largest 5 account for 25% of the ETF. If you want to investigate them further, they include TFC 0.00%↑ , MTB 0.00%↑ , RF 0.00%↑ , HBAN 0.00%↑ and CFG 0.00%↑.

Last month, banks in the US and globally got into trouble as some of them could not handle deposit outflows anymore. Attractive conditions in the money market have drained the entire US banking sector by $1tn worth of deposits over the past year.

It’s an ongoing crisis that has not been resolved yet. It’s preliminary peak was the collapse of Silicon Valley Bank on March 10, 2023. More recently, we have seen negative results from First Republic Bank FRC 0.00%↑. They lost 35% of their deposits during 1Q23. The stock just limped into the weekend, down 75% from Monday morning.

Out of Investor Favor

As of February 2023, fund managers were overweight banks by more than an entire standard deviation vs. historical standards.

We can only speculate about the reasons for this overweight. But it is likely related to their strong profitability facilitated by stale deposit rates in conjunction with surging interest rates.

Then Silicon Valley Bank happened. And Boom! Now they are considerably underweight.

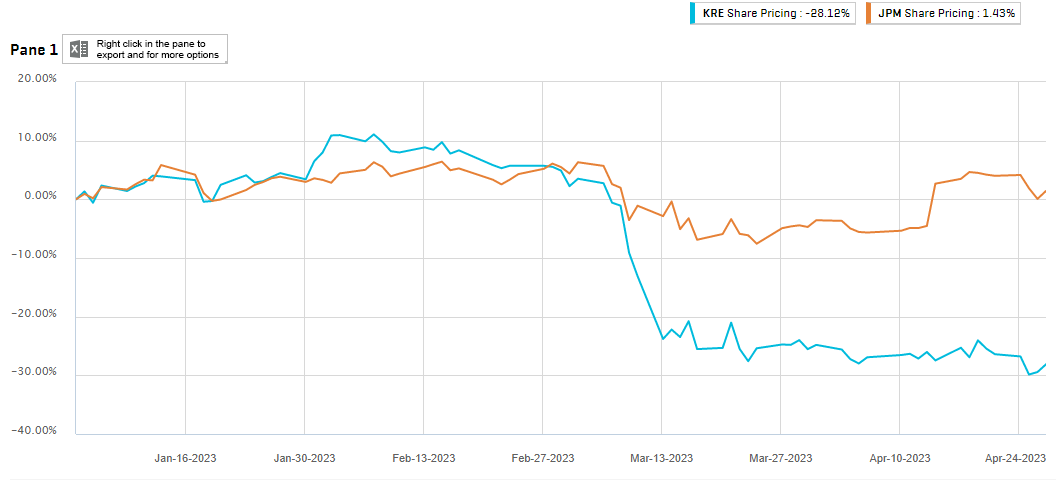

And to the extent, they do still own banks, they are in the big ones. Here is JPM 0.00%↑ vs. KRE YTD:

As a professional money manager, it is now a career risk to own regional bank stocks. Their super slow motion car crash is one of the most widely covered crises out there. It seems like it’s only a question of time until the next institution blows up. Do you really want to explain to your boss why you are part of that blow up?

Investors are actually not just avoiding regional banks. In fact, there are a lot of traders actively shorting them. KRE short interest is 2x above historical levels.

There is little we can infer here with respect to a potential industry-level short squeeze because KRE is an ETF that represents <1% of the aggregate market cap of its constituents. But there are some heavily shorted stocks in this ETF.

The market value-weighted average short interest on all constituents is 4%, which twice the level of the S&P.

Is this pessimism warranted? To assess that, we need to understand how to value banks.

A primer on bank valuation

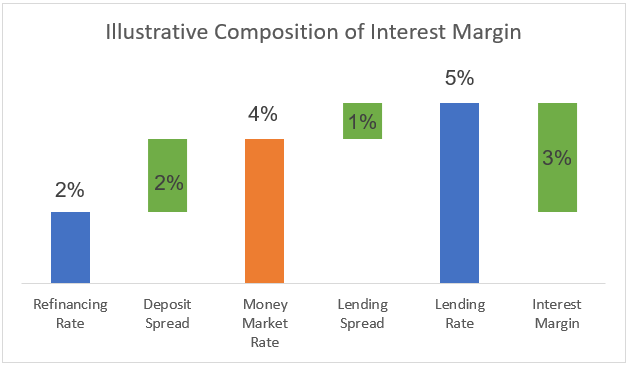

A traditional bank creates value by providing a digital and physical infrastructure to attract (and retain!) deposits. It is the foundation of their business model because it is the cheapest form of refinancing. They can then use their advantageous financing mix (consisting of deposits, financial debt and equity) to lend money at a higher rate and/or invest in higher yielding assets. The difference between the interest they pay and the interest they earn is called interest margin. They have two levers with respect to this interest margin:

Deposit Spread: Refinancing savings on their deposits vs. alternative cost of funding via interbank market or Fed lending for example.

Lending Spread: Deploy funds into assets with higher yields than the interbank market (corporate loans and bonds, consumer loans, credit cards, etc.).

On top of the interest margin, they will also generate capital gains or losses on their asset portfolio, primarily driven by changes in interest rates, credit risk spreads and default rates.

In addition to that, they can leverage their relationship with depositors and debtors to sell additional financial services to them, such as selling insurance policies, offering securities brokerage services or providing corporate finance advice.

The better they do all of this, the higher their valuation premium vs. their equity book value will be.

The chart below illustrates the combined bank valuation consisting of:

Equity Book Value: Book value of assets minus book value of liabilities

Mark-to-market adjustment of assets and liabilities (capital gains/losses)

Present value of future interest margin earned

Present value of all additional financial services

On-Balance and Off-Balance Sheet

A bank balance sheet provides an incomplete picture with respect to their financial position. Typically, banks have a lot of assets (and potentially liabilities) that are not recorded therein. These can include for example technology/process know-how, customer relationships or brand, all of which may enable them to provide and grow financial services at lower cost or higher quality. Some of this may be recorded in the balance sheet due to past M&A, but a lot of it is usually hidden. Markets care about these hidden assets. That is why they typically trade significantly above their equity book value.

This is important to note when people argue for example that a bank’s unrealized losses on their assets wipe out their equity. That is primarily a regulatory question and regulators give them a pass with current accounting standards, like held-to-maturity.

Having established this framework, there are a couple of metrics we can derive to gauge how ambitious or unambitious banks are valued at the moment:

Deposits: As outlined above, banks utilize their digital and physical infrastructure to attract and service deposits, which enables them to earn a positive interest margin. Therefore, the market value of the equity of a bank should be a function of the deposits.

P/TBV: The better banks deploy their funds (from equity, debt and deposits) into interest-earning assets (loans, securities) and non-interest earning assets (equity investments, real estate, customer relationships), the higher their market value should be vs. their (tangible) book value.

Where do we stand on those metrics vs. historical levels?

Deposits

Over the past 15 years, the combined KRE 0.00%↑ market cap was on average 17% of the combined deposits administered by these banks. If you deposit $1 with your bank, that is worth $0.17 for their shareholders. That's why they give you a TV to open an account. You're a gold nugget to them.

It was much higher at 22% in 2007 shortly before the GFC. And it was the highest ever at 25% in January 2018. That was at the tail end of the strong mid-2010s bull market with a healthy upward-sloping yield curve causing a large spread between deposit rates and lending rates.

Today’s 11% is on par with the 12% in June 2020 and 9% at the height of the GFC in January 2009.

P/TBV

P/TBV paints a similar picture. It used to be 2.5x before the GFC. Since then, it has averaged 1.6x. Today, we’re at 1.3x, close to the March 2020 Covid-bottom (1.1x) and the January 2009 GFC bottom (also 1.1x).

So, the valuation of regional US banks is very unambitious. That is unsurprising. But it leads to an interesting follow-up question.

Is that valuation discount fair?

Is the outlook as bleak as it was in the spring of 2009 and the spring of 2020? To maintain a healthy business model, banks need to be able to a) attract and retain deposits, b) earn a positive interest margin, c) not lose money on their assets (capital losses or customer defaults) and d) earn income on their additional services. So, how are those things going?