🔎🔥Let's bet on Oracle 2.0, shall we? (incl. Excel workbook)

They are well-positioned to succeed against hyperscalers and neoclouds. And their cloud business differentiates them from pure software companies the moats of which are eroding. The ideal AI stock?

Earnings summary

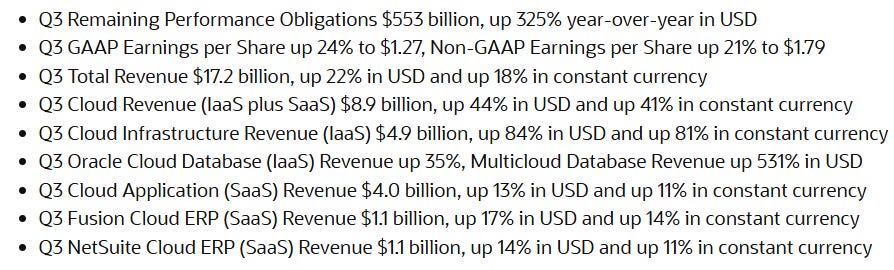

Oracle just reported 3Q26 earnings. They generated $17.2bn in revenues (up 22% YoY) and $5.5bn in operating income (up 25% YoY). More importantly, they reported a continued acceleration of their remaining performance obligations. These now stand at $553bn (+325% YoY). The initial reaction of the stock is positive. I believe a narrative shift is in the making here. Oracle is transforming into possibly the most profound hypergrowth story in the megacap space since NVIDIA three years ago. Don’t be asleep on this.

What follows below is a big article to contextualize Oracle’s performance and competitive position in the AI investment theme. There are lots of numbers and tables in this article, most of which are included in the attached Excel workbook. If you disagree with any of the assumptions, check out that workbook.

Enjoy!

TLDR Summary

Let’s face it. There won’t be an AI capex slowdown. Most companies will keep spending even if weak economics persist because the alternative to spending is losing their business. The main feat of AI is that lowers entry barriers in many industries. New entrants will challenge incumbents who will desperately try to defend their businesses against those newcomers and against each other.

Therefore, the AI cloud industry will likely meet or even exceed expectations. By 2030, it might generate $1tn in revenues and $300bn in gross profits. Oracle is in an ideal position to capture a sizable chunk of that industry.

In contrast to neoclouds, they have a huge legacy business that can serve as collateral to fund the data center build out. Cost of capital advantages matter greatly. Neoclouds also don’t have the software integration that makes Oracle a natural cloud provider.

Hyperscalers have an even lower cost of capital than Oracle. But they are much more ambitiously valued and they have a higher risk exposure. Oracle is not invested in AI cloud customers in the same way hyperscalers are. They operate with a safety net. If the entire AI industry had one balance sheet, Oracle is its most senior tranche.

The company’s strategic pivot also conveniently shields them from the troubles of the SaaS industry. Software moats might evaporate. Capital moats won’t.

Overall, this is a fascinating setup. The company is finally playing its cards well. They will likely play a major role in the hottest innovation theme of our time. And they don’t seem to be priced as such. Yet.

What is Oracle 2.0?

Oracle shocked the stock market in September 2025 when they revealed a 359% increase of their remaining performance obligations (RPO). It was later reported by the WSJ that much of this related to a five year deal struck with OpenAI. This deal catapulted Oracle from the fringes of the cloud industry to its very center. A redefining moment for the company.

ERPs like Oracle were destined to play a major role in the cloud industry from the beginning. They are the record keepers for large enterprises. Every business process runs through them. This gave and gives them great insight into corporate processes and it makes their services very sticky once they are in. Even before AWS conquered the world, it would have been a great selling point for Oracle to tell their customers to remove their costly and complex on-prem systems and simply subscribe to a cloud service. Unfortunately, they were asleep and missed out.

AI computing provides an opportunity to rectify this mistake. As Oracle 2.0, they won’t just document the operations of their customers anymore. They will actively run them. They will host an increasing share of corporate functions and workflows, ingraining themselves even deeper into the internal processes of their customers.

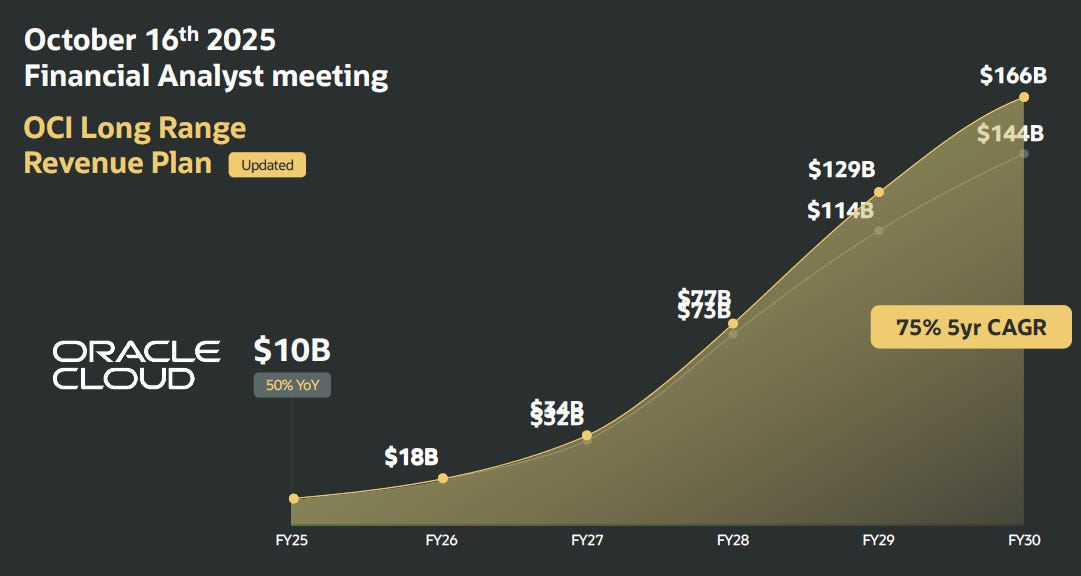

This transforms the company into a massive growth story. Over the last ten years, Oracle has grown their topline by a pitiful 4% annually. Now, they are guiding their cloud business to grow from $10bn in 2025 to $166bn in 2030. That’s about five times (!) their entire ex-cloud business today.

The stock went vertical immediately on that news and surged 35%. One of the largest one-day market cap jumps in history. The vibes on the analyst call were ecstatic.

However, Oracle stock has given up all those gains and more over the months that followed. Today, it’s even 30% lower than before those blockbuster earnings, implying that the much celebrated strategic pivot revealed in September 2025 will actually have a negative net present value.

In particular, investors are concerned about the enormous capital requirements and the stress these put on Oracle’s balance sheet. Also, it has become very fashionable for investors and customers to hate OpenAI, the reputation of which is similar to Facebook in 2013. Oracle’s association with them is a valuation burden. And lastly, the broad software sell-off isn’t helping either.

It’s worth revisiting the stock in light of this volatility. Today’s earnings announcement is a great opportunity to do so.

Before I go into Oracle specifically, I want to provide you with some top down thematic framing first. My curiosity about Oracle is very much driven by my overall perception of AI as an investment theme. The firmest statement I can make about it is this: