LMND 2Q23: Still an excellent short idea

Lots of promises with little tangible progress against their mission. Not a broker, not a carrier. How do they plan to ever make money?

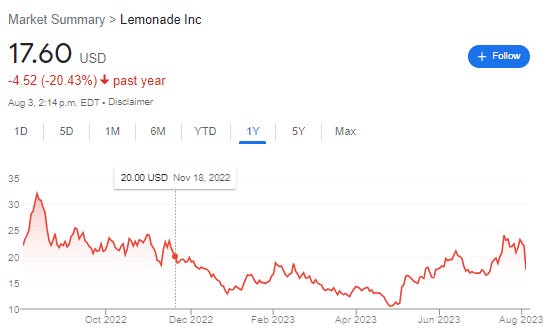

Yesterday, Lemonade LMND 0.00%↑ published their 2Q23 earnings. Markets did not like this release at all. Today, the stock finished down more than 21.6% to $17.31.

On Nov 21, 2022, I published a report on Lemonade as a short idea:

I explained why I have doubts that their strategy will eventually yield sufficient profitability, why I have doubts about management’s ability to succeed with their mission and (even if they do) why I think their financial planning sets them up for falling market capitalization and likely substantial dilution. Looking two to three years ahead, I saw the stock heading sub $10 if they don’t get bought out first. This implied 50% downside as the stock was trading at ~$20. To fully appreciate this 2Q23 earnings coverage, I encourage you to read that report first.

It seemed I was proven right quicker than anticipated given the stock plummeted to $10 over the coming 5 months. However, to be fair, most of that was driven by a bad macro environment for growth stocks and financials. Over the subsequent months, the stock surged back to $24 driven by improving macro sentiment and supposedly encouraging 1Q23 earnings. I believe today is a good point in time to revisit my short thesis.

The numbers

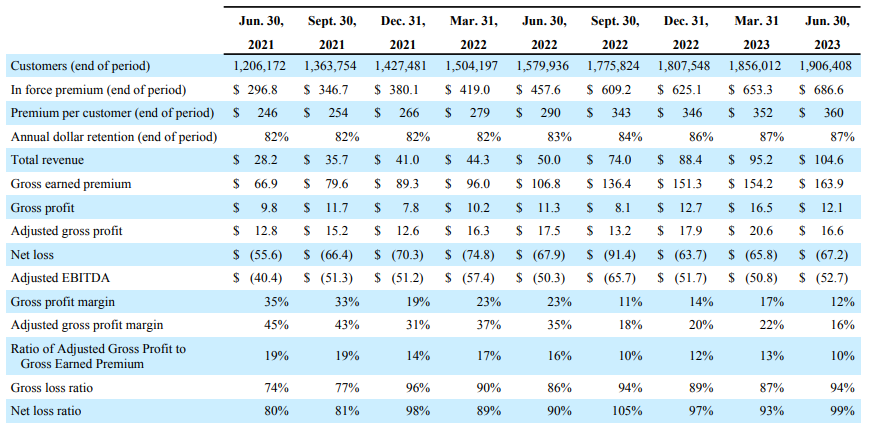

At first glance, it does not look that bad. Revenues doubled year over year and in-force premium is up 50% year over year.

But there was barely any improvement on profitability and that is the central aspect of the bull case. The net loss ratio came in at 99% which is far above industry standards. Most competitors operate at 55-70%.

Lemonade claims that this will improve over time as their customer portfolio matures and positive impacts from their AI investments will materialize.

But I sense a severe disconnect between this bull case and financial services reality. Financial services are commoditized services with the price being the most important driver for market share. That makes financial services for the most part supply constrained. You can always generate more revenues by undercutting your competition.

To demonstrate the merits of their business model, Lemonade has to a) show strong volume growth to validate the growth story and b) be very restrictive with customer selection to allow their AI to enact its power. These are clearly conflicting goals. I believe management will prioritize the former when they face this decision because that is obviously where the story would break first. In my opinion, they have made this choice already with this earnings release.