🔎Momentum Trifecta

Three feedback loops are driving the most dominant factor regime ever. Understanding that doesn't need to make you bearish. But be aware of them to realize when the music stops playing.

TLDR Summary

Since late 2023, Momentum has been outperforming all other investment factors with a persistency and a dominance that has rarely been observed before. The convergence of three feedback loops makes that possible:

Interest Loop: Interest expenses are now accounting for 60% of the Treasury’s deficit. This converts the fiscal impulse from a means of countercyclical liquidity creation to one of procyclical liquidity creation: The higher the Treasury’s interest rate, the higher its deficits, the higher the growth of nominal GDP, the higher the interest rate…

Corporate Loop: Bull markets and times of prosperity are usually driven by household consumption. Companies earn more when household incomes are rising or when households are borrowing to spend. The bull market of the 2020s is different. Companies are creating their own demand: The more debt and equity they raise, the more they will spend, the more will corporate earnings grow, the more will investors demand their debt and equity, the lower their cost of capital will fall, the more debt and equity they will raise…

Flow Loop: Trillions of investment dollars are being converted from active into passive mandates. In contrast to active investing, passive investing is valuation indifferent. That makes previous price performance the best predictor for prospective performance: The more the price of an asset appreciates, the higher its share in the most popular ETF baskets, the larger the share these ETFs will allocate to that asset, the more it appreciates…

Momentum, Momentum, Momentum

In August 2025, I wrote the article below describing the Momentum Bubble, where I linked the remarkable outperformance of the Momentum factor to fiscal liquidity creation and to the rise of passive investing. The Treasury’s excessive deficit creates savings for investors which these are then increasingly allocate into valuation-insensitive passive mandates. As a result, trends become stronger and last longer, fertile ground for Momentum factor investing.

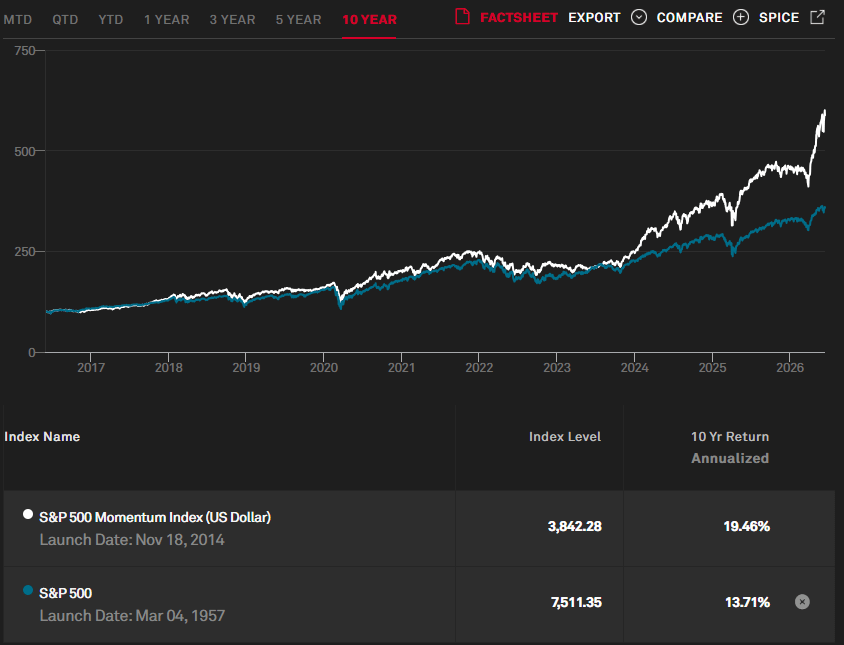

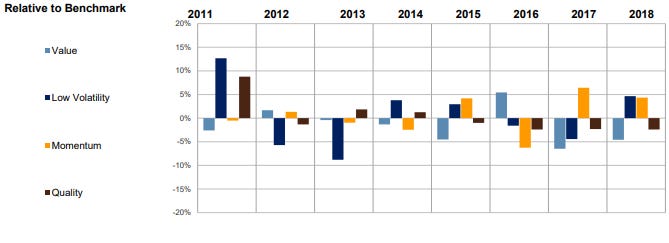

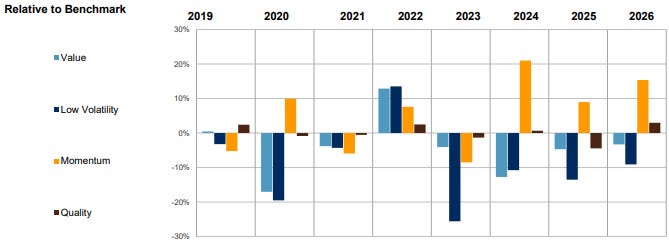

This theme keeps dominating, in fact it seems to be escalating. The current Momentum regime started in late 2023. Before that, Momentum didn’t systematically outperform for many years.

The S&P 500 Momentum Index is up 160% since then (+44% p.a.), while the S&P 500 is up ‘only’ 72% (+23% p.a.). More than 20% outperformance per year for a single factor. I’m not sure if any factor has ever dominated that much, but certainly not in the last 15 years.

For Momentum to perform and to sustain, there must be circularities in place that reinforce existing trends. Outputs of a mechanism must become inputs for the same mechanism. In my opinion, there are three of such feedback loops that are driving the current momentum regime.

1) Interest Loop

US GDP is currently closing in on $32tn. At the same time, the US Treasury net spends $2tn per year. That’s still more than a 6% deficit, unprecedented outside of recession periods. The 2020s have to be viewed as a fiscal experiment of gargantuan scale.

The Treasury deficit is actually designed to act countercyclically. Tax receipts typically grow in proportion to nominal GDP growth (i.e. real growth plus inflation) . Outlays typically grow in proportion to inflation because much of the spending is subject to price adjustment clauses. Therefore, the deficit typically shrinks during times of positive real growth, acting as a counterforce to potential overheating. Likewise, it typically expands during recessions when tax receipts falter and costs for unemployment insurance increase.

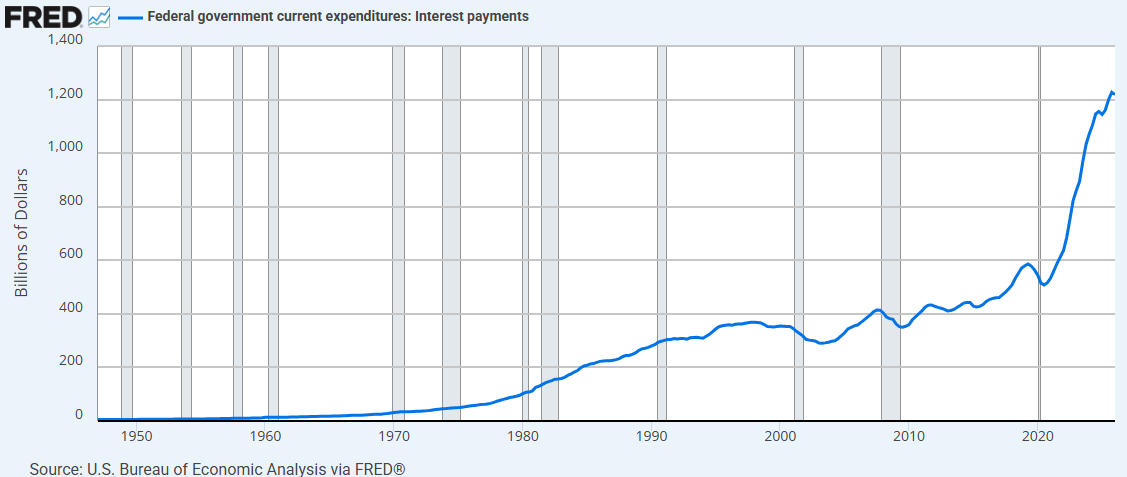

In the current fiscal dominance regime, this is not the case anymore because of the rising importance of interest payments, which now account for $1.2tn annually or 60% of that deficit. They have more than doubled since before the pandemic.

Why does that matter? Because fiscal deficits are first and foremost private sector savings injections. The type of deficit may matter out of fairness/justice considerations. At the aggregate level it doesn’t matter. Social security payments or military spending accomplish the same thing as interest payments: They give money citizens, companies or foreigners with an economic interest in the US. And those counterparties will then use that money to create demand in other pockets of the economy. Deficits drive nominal GDP, whether its real growth component or its inflation component.

And that nominal GDP is also the main driver for interest rates. Bond investors demand interest to compensate them for opportunity cost (they could have invested in assets with a higher beta to real growth) and for inflation (the debasement of their principal). This closes the circle: The higher the Treasury’s interest rate, the higher its deficits, the higher the growth of nominal GDP, the higher the interest rate…

2) Corporate Loop

Generally speaking, businesses will do well when their customers are spending. Customers can either spend their current income or their savings (or going into debt). Therefore, corporate earnings typically rise either when household incomes are rising or when households are borrowing. The 2010s were an example of the former, the 2000s were an example of the latter.

The bull market of the 2020s is different from the 2000s and 2010s in that it’s not being led by household spending. It’s being led by corporate spending. B2B businesses are leading this bull market, primarily in the AI space. They do well when other companies are spending. Absent of a demand impulse at the end customer level, these companies can only increase their spending by tapping into equity and debt capital.

They are encouraged to raise equity or debt when the cost of that capital is low. And the cost of that capital is low when there is a lot of investor demand for it. Investors are the new customers in the 2020s. This closes the circle: The more debt and equity companies raise, the more will corporate earnings grow, the more will investors demand their debt and equity, the lower their cost of capital will fall, the more debt and equity they will raise…

3) Flow Loop

Active investors are valuation sensitive. They won’t buy an asset if they deem it to expensive for the cash flows it generates. In contrast, passive investing is valuation indifferent. It validates any prior price because it simply enters ‘market buy’ orders for every asset weighted by its current market cap. This amplifies mispricing to both upside and downside. Stocks don’t run out of buyers/sellers when they rise/fall too much. Instead, a rising stock automatically gets a larger bid the next day. This closes the circle: The more the price of an asset appreciates, the higher its share in the most popular ETF baskets, the large the share these ETFs will allocate to that assets, the more it appreciates…

Sincerely,

Rene