🔎Short the banks?

Valuations are too stretched. Yield curve steepening expectations will likely disappoint.

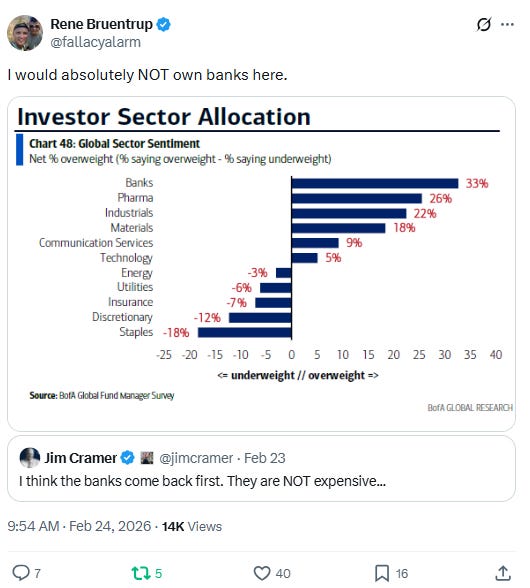

This article would have been more valuable if I had gotten to it a month earlier. Apologies for that. But I believe it’s still a hot topic though. In my opinion, the rotation out of banks stocks has just started.

TLDR Summary

Bank valuations are stretched. The four largest US banks are trading at a weighted average P/B multiple of 1.5x (vs. 1.0x last 10 year average) and 19x P/E (vs. 12x last 10 year average).

Investors expect a cyclical acceleration of bank earnings, most likely from a continued steepening of the yield curve. Banks typically borrow short-term and lend medium/long-term. The steeper the yield curve, the stronger their net interest margin should be in theory.

The steepening thesis is predicated on the idea that the Fed will cut rates into a robust macro environment. Rate cuts would then lower the short end of the curve and their inflationary impacts would raise the long end. It’s part of the Debasement Trade. The dominant macro theme of the last 12 months.

It’s a flawed thesis. In my opinion, the 10-Year Treasury yield has not held up so strongly because rate cuts are expected to reignite inflation. It has held up because of the robust growth of the US economy due to the AI capex boom. This capex boom may very well continue. But it will be more challenging going forward to keep GDP growth high.

And even if the yield curve get steeper, bank earnings won’t necessarily benefit as much as investors seem to hope. The steepening of the last two years has actually done very little to the net interest margin of banks.