Shorting UVXY: Madness or Money Maker?

Bearing volatility is the only way to systematically generate returns. The most explicit way of doing so is by directly shorting the VIX and exploiting its Contango futures term structure.

Before we dive in: I recently discussed Tesla’s Q2 earnings with Randy Kirk. We touched on the cyclicality of their margins, the strategy of the Legacy OEMs, the ramp of Tesla Energy and insights from option trading. Check it out and let me know what you think!

Volatility is a nasty thing. Many people try to hide from it. Without doubt, the obsession about avoiding volatility is right up there with procreational and tax minimization instincts. It probably even beats both of them by a decent margin.

Think about a stop loss for example. Theoretically intended to avoid drawdowns, actually designed to avoid returns. The moment you implement a stop loss, you have already determined the price at which you will eventually sell. Mr. Market will find your stop loss and exploit it. Buying puts is another example. Sure, it may work as a well-researched speculative bet. But in general, buying puts has a negative expected value.

Unless you have a very special edge, there is only one way how you can systematically make money in investing: You need to bear volatility. You need to be exposed to it. You need to suffer when it rises. In finance lingo: You need to short it.

Buy & Hold is the most basic and implicit form of shorting volatility. When there is none of it, equities just earn their cost of capital and you will compound at 5-10% annually. When volatility enters the stage, you will suffer drawdowns. Bearing these drawdowns without selling into weakness will over time pay the equity risk premium.

On top of Buy & Hold, there are also explicit short volatility strategies, like call and put writing for example, some of which I have covered before.

Today, I want to cover the most explicit form of shorting volatility: Shorting the VIX, the most famous volatility gauge in the world. The vehicle I will look at to do so is UVXY 0.00%↑, an ETF that buys VIX futures contracts. I will cover the following four questions:

What is the theoretical foundation for shorting volatility to be profitable?

How profitable has it been in the past?

Is this a good moment in time to short volatility?

How am I implementing a short volatility trade?

Shorting volatility is equal to providing liquidity

Functioning markets require liquidity providers. That is particularly true in financial economies that employ leverage because liquidity is scarce when debt is high. Shorting volatility provides liquidity when it is needed to achieve market clearance. Investors with the ability and willingness to buy the dip reduce volatility. That makes the financial economy more reliable with positive impacts on the real economy.

Therefore, shorting volatility must have a positive expected return to compensate liquidity provision. This is evidenced in the success of explicit short volatility strategies like writing covered calls and puts.

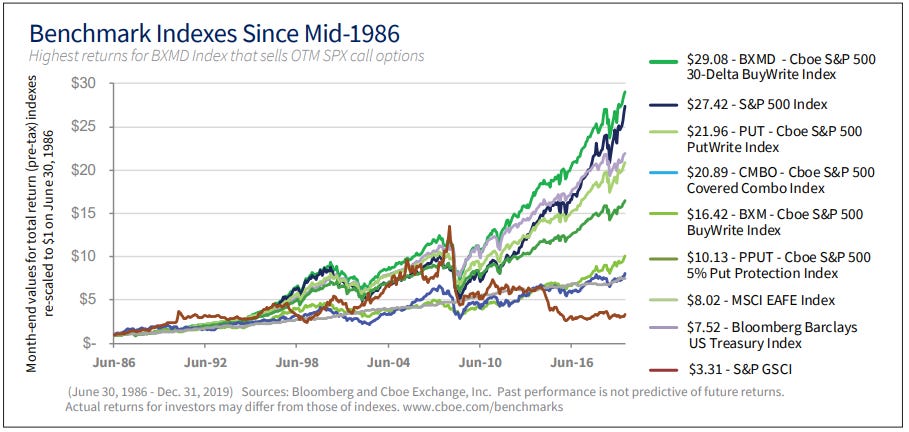

The CBOE maintains benchmarks for certain option strategies. Buy Write (stock + covered call) and Put Write (cash secured short puts) strategies are the most common short volatility strategies and should in theory achieve similar results. As demonstrated below, they generally have a positive expected return and they perform by and large in line with a simple Buy & Hold strategy. Some even outperform over time and/or have a better risk/return profile.

Trading VIX futures is the most explicit form of shorting volatility. It’s a delicate strategy, but it can be very profitable. The reason for that can be found in the slope of its futures term structure.

The VIX Term Structure

A futures term structure can be upward sloping (Contango). Then expiry dates further out will be more expensive. Or it can be downward sloping (Backwardation). Then expiry dates further out will be cheaper. The VIX futures term structure is typically in Contango because the sellers of volatility futures demand a positive roll return.

Why can they claim that roll return?

Implied volatility has two key characteristics. Firstly, it’s stationary and mean reverting. Whether it rises or falls, you know it will come back. And secondly, it’s right-skewed with a low base level that is interrupted by upward spikes which can be fairly violent.

Over the past 30 years, the median VIX has been 18, while its average has been 20 due to the frequent spikes. The VIX has been tracking 20-Day realized volatility fairly well. Its median has been 13, while its average has been 16.

As a result of these two key characteristics, the volatility seller has a very unfortunate payout profile. Most of the time, there is barely any further downside while upside risk is enormous. So, in order to entice the seller to enter into a trade for a futures contract, they need to be compensated with a positive roll return. For example, why would you as a seller enter the December contract today at 14 when the spot VIX is 14 and historical median volatility is 13? There is barely anything in it for you. So the volatility buyer will have to lure you in by paying you a premium. If nothing happens, you need to be paid. That’s the core principle of shorting volatility.

An insurance carrier is a great analogy for this purpose. The reason why you buy insurance for your house is because you don’t want to or can’t afford to lose your house in a fire. The insurance carrier can afford to pay due to their strong balance sheet. Let’s say your $1m house will burn down with a probability of 0.1% next year. Why would the insurance carrier enter into an insurance contract for $1,000 when they are at risk of losing $1m? You will need to pay them a premium on top of the expected loss to make it a compelling transaction for them.

For these reasons, the VIX futures term structures exhibits one of the steepest positive slopes of all futures markets out there. How can that be exploited?