The Demographic Deflation Bomb is ticking

The eroding demographic base encourages the resumption of QE, will bring us back to a stagnating, low inflation environment & reward investors for betting on the scarcest of all things: Growth!

The podcast version of this article can be found here.

You cannot see it in aggregate population numbers yet, but we have been dealing with an undermining demographic base for 40 years, which is a major headwind for economic growth. It dampens demand for goods, services and infrastructure. A huge deflationary force that has been brewing for decades. And while the topic itself is fairly well known, its economic implications continue to be vastly underappreciated.

Policymakers (both fiscal and monetary) have been scrambling to fill this structural and widening demand deficit with massive quantitative easing programs over the past 15 years. They did not just do it to mess with savers and creditors. They had to do it in order keep the current economic system going.

In this article I will argue that what they have been doing is the rational choice, one could even call it the right thing to do. They will do it again. We will be back to an anemic growth, low inflation environment quicker than many people think. And it will fuel asset prices for those stocks that offer what is scarcest: Growth!

The Great Baby Bust

For the analysis below, I have selected High Income Countries (HIC) as defined by the World Bank plus China. HIC include the 45 countries globally with the highest GDP per capita. These are home to approximately 1.3bn people and account for 40% of global GDP. China is home to 1.4bn people and accounts for 16% of global GDP. So together HIC+China represents the 2.7bn people on earth most relevant for the economic process as they are responsible for 56% of global GDP. The trends you will see below are happening in many more places in the world, it is just the most progressed for HIC+China.

Let’s take a look at their current age structure:

The age cohort of 0-4y olds in HIC+China included 150m people in 2020. This is 30% smaller than the current size of the peak generation of the 30-34y olds (the infamous Millennials I have mentioned often in this newsletter).

And it gets worse.

Here is the projected age structure 10 years down the road based on the United Nations’ Low Variant Scenario.

The 0-4y age group is projected to include 105m people. A whopping 50% smaller than the peak Millennials. If this trend continues, it is quite simple to make the case for the entire HIC+China population to drop by 50% in the long run. Are you living in any of these countries? Imagine removing every 2nd person you encounter in your daily life. How would that look like?

Why the Low Variant Scenario?

The United Nations maintain long term population projections in three scenarios: Low, Medium and High Fertility. At this point, we are most likely tracking towards the lower end of that range.

I highly recommend to read Empty Planet written by Darrell Bricker and John Ibbitson which makes a compelling case why population will likely undershoot expectations in the coming years and decades.

The essence of their argument is this: The United Nations’ population projections are based on the assumption that high fertility countries of today will track towards lower fertility at a speed similar to today’s low fertility countries. For instance, if it took Germany 50y to go from 4 children per woman to 2, it would take the same time for Nigeria.

However, today’s high fertility countries in Africa and Asia will likely drop much faster compared to what happened in Europe, North America and Developed Asia over the past century due to much higher urbanization levels and female empowerment. Compared to a rural, agricultural environment, kids are not assets, but liabilities in urban environments, which disincentivizes large families. And the more women receive education and increase their ability to earn income, the less they are subject to male dominance and the less they are likely to agree to having many children.

In addition to that, there is a bias in the projections performed by the United Nations. Over many decades, overpopulation was a big issue for humanity. At certain times during the 20th century before the advent of birth control at large scale, projections were frightening. It became a global effort to get population growth under control. In many parts of the world, the battle to get birth control and family planning on people’s minds is still very much ongoing. This is why the UN have an incentive to overshoot with their projections to keep a sense of urgency to this issue.

The eroding Demographic Base drives the Debt Binge

I have covered the Great Fiscal Debt Binge in the article below, where I mainly associated the chronic growth of public debt with moral hazard of fiscal policymakers:

But I think there is more to this. We have not been hit with deficit addicted politicians by chance. There is a reason.

Our economic system is designed for real growth of aggregate economic output. This gets increasingly difficult as the population is shrinking. We can not see it yet in the aggregate population numbers because human lives are long and the large generations are still here with us. And in many countries, immigration will continue to prop up numbers for a while before the source countries run into the issues from their own baby bust. But ultimately, 30-50% less children in Generation Alpha vs. Millennials means 30-50% less kindergartens, schools, need for teachers and later professors. And who will buy all these homes 10, 20, 30y down the road?

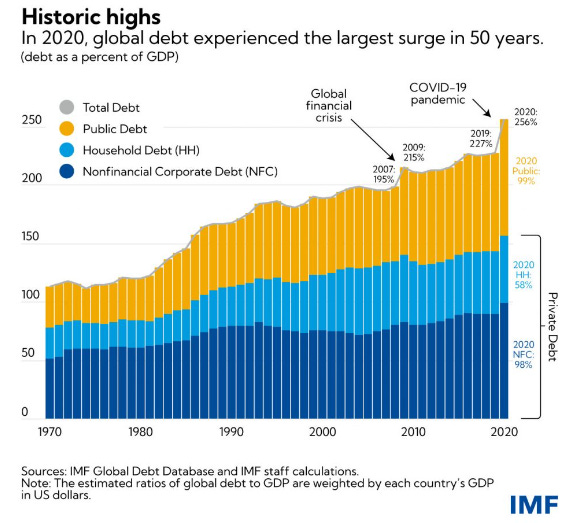

HIC+China have been dealing with an eroding human base for 40 years. During these four decades global total debt to GDP has risen from just over 100% to above 250%.

As natural demand for goods, services and infrastructure has been vanishing, our economic system has been called into question several times. And in an effort to keep it going, policymakers have taken bigger and bigger sips from the debt bottle, effectively propping up present demand with future demand. You need a car tomorrow? Why don’t you buy it today on credit instead? And we will worry about who will buy tomorrow’s production capacity when time comes. By the way, deficit funded EV tax credits are the same thing as cars financed through consumer credit from this aggregate perspective.

If you want to find persistent inflation going forward, look for true scarcity.

You might argue: Well, less people does not only mean less demand. It also means less supply. It is the balance of those that matters for inflation.

And you’d have a point. The chart below shows the ratio of people in productive ages (20-64) to people in dependent ages (<20 & >65), which is pivoting right now:

In my article about the Great Inflation, I have argued that Young Dependants are more inflationary then Old Dependents:

The age structure in an economy plays an important role to determine the balance of inflationary and deflationary forces. People at productive ages (say 20-65) tend to cause deflationary pressure. They are net savers because they earn more than they consume to save for retirement. On top of what they earn, they typically also contribute to capital returns because the value creation in their jobs typically exceeds what employers pay them. These excess savings/lack of consumption drives down interest rates and inflation.

In contrast to that, people at dependent ages (<20 & >65) consume more than they produce. They depend on the people at productive ages to take care of them. There is a difference though between those <20 and those >65. The former group increases their excess consumption every year. Even though young parents might adamantly disagree, a teenager consumes more resources than a toddler. Those >65 decrease their excess consumption every year. You might go on a cruise at 66 and play a lot of golf. Likely you won’t do that anymore at 86.

But I do have sympathy for the argument that an ageing society might experience inflationary pressures as labor becomes scarcer and hence more expensive. But labor is only one input factor. Capital is at least as important and its importance grows with automation and digitization. Factories are already built and will not disappear overnight. There will be less housing construction because there will be an excess supply in existing homes once the current wave of Millennial home buyers is through with it.

Sure, the price for getting a haircut or to hire a plumber will continue to rise. But what were the biggest drivers of the 2022 inflation spike? Vehicles, commodities and energy prices. Highly capital intense economic goods with little labor input. Hard to believe these can sustain rising prices in an economy that slowly but surely adjusts to a lower footprint.

Goods and services that are highly labor intensive and challenging to automate may have sustained inflationary pressure. Anything that requires human relationship skills. But there will not be broad based inflation in goods and services without true scarcity features. If there is no reason why you can’t make more of it easily, its price will not inflate.

Monetary policymakers are not doing QE due to moral hazard, they are pressured to do so based on economic forces.

If you have read my About page, you know I try to view the world as it is, not as I want it to be. But for the longest time, I could not help but being critical of the large 2010s QE programs. I found them flat out wrong and unfair. It felt like investors and debtors were taking advantage of savers and creditors. But in recent weeks I had an important revelation:

There is a chronic and widening demand deficit in our economy that stems from the eroding demographic base. Yes, it can be overshadowed by cyclical forces as we have seen in the past two years, but it is always there, influencing the economic process under the surface.

This demand deficit is an extremely underappreciated deflationary force that has erupted to the surface in the 2008/09 Global Financial Crisis. And has remained with us since then. In order to tame it, Western central banks have expanded their balance sheets like never before. Together, USA, China, Euroland and Japan have 4x’d their balance sheets in the 10y after the GFC:

And what has happened to overall money supply growth? It was actually below its long term average for most of the 2010s. Bank lending, the other important liquidity driver, had several periods where it effectively contracted over a 3y period:

Central banks are desperately trying to replace this demand deficit. And along the way, they are bailing out investors and debtors at the expense of savers and creditors. But why are they doing that? Is it perhaps endemic to this demographic set-up?

Is the advantaging of investors/debtors over savers/creditors systematic with eroding demographic base?

Here is an important mental model I am using when I assess things that happen: 99% of what monetary and fiscal policymakers do is financial engineering. They transfer economic resources from one party to another, they are not creating any wealth. They just cut the pieces of the pie for everyone.

If they let the economic process run course, i.e. no QE and no structural deficits, the economy in its current shape will run into a deflation spiral. Even with stagnating wages, people will become wealthier in real terms. Everyone participates in the fruits of the economy even if they don’t own equity in any corporation.

By artificially inflating the currency against its natural gravity, policymakers shift economic resources from savers and creditors to investors and debtors. Unfair you think?

Here is the catch: It is rational to do so. And it is the right thing to do! At least in the right dose.

In a world with natural deflationary pressures where we keep getting better at making things and will need less things because there will be fewer of us, nobody would actually invest into equity or take on a loan to start a venture. Why would you? You will participate in economic returns anyway because you will be paid in appreciating Dollars, Euros, Yuan or Yen.

So, to keep the economic process running, investors and debtors HAVE to be incentivized invest equity and raise debt. I could even argue that it would be unfair not to do so. Why should savers/creditors participate in economic upside through deflation if they do not take any risk?

In an economy with anemic growth due to an eroding demographic base, negative real interest rates can be viewed as a risk premium to compensate investors/debtors to do what they do against rational choice. Likewise it is tax on savers/creditors for penalize them for making the rational choice.

Incentivizing investors and debtors is precisely what policymakers have been doing for the past 15y. Yes, they have overdone it with their reaction to the plague, but once that shock and its countershock is churned through the system, we will return to the 2010s world. My conviction in that is actually extremely high. What do you think?

"We will be back to an anemic growth, low inflation environment quicker than many people think. And it will fuel asset prices for those stocks that offer what is scarcest: Growth!"

How is a dire situation somehow positive for investment? If growth is anemic, how can there be growth stocks? And how can investments get 'more valuable' the more dire the situation gets? I think it goes on a long time like Japan but eventually you get a hyperinflationary collapse. Japanese yen is already falling off a cliff.

great article!!