What might Tesla's 2023 EPS look like? (Excel Model included)

Bridging LTM EPS to 2023 by considering volume growth, price cuts, FSD take rate, Semi, Energy and Interest Rates.

In my last article, I have argued that Tesla’s valuation has transitioned from (unprofitable) explosive growth to GARP (Growth At Reasonable Price). This gives two metrics outsized relevance in its price discovery process: P/E and EPS.

For the first time in its history, its EPS is significant enough to build an investment case based on earnings and assigning a multiple to it. You can observe this phenomenon when you compare public discourse about the stock now vs. two years ago. Very few people talked about P/E and EPS back then. Today, those metrics often take the centerstage.

In that article, I have build up a case why Tesla should trade at 50-60x P/E to reflect its competitive positioning and visibility of the growth story. The logical next step is to develop an EPS estimate for this multiple. In this article, I will attempt to do so for 2023.

2023 Consensus EPS has risen sharply over the past three years from $1 to >$5. But analysts have revised their estimates down recently, presumably driven by uncertainty relating to demand raising doubt on the company’s ability to grow production as planned and defend margins.

As of today, consensus stands at $5.22, which would be a 29% increase over the estimate for 2022 ($4.05). For clarification, this refers to Normalized EPS. In Tesla language: EPS attributable to common stockholders, diluted (non-GAAP). It removes stock-based compensation. I am not overly happy with that convention since shareholders pay for that compensation via dilution. I view that as a cash-like expense. But have made my peace with it long time ago. It is just easier to work with the numbers everyone is working with and an argument can be made that it is self correcting as long as we select a multiple based on a comp set with equally normalized EPS estimates.

I will be doing this a bit differently compared to what you might expect and might have seen from others. I don’t have the capacity to build up income statement projections bottom up properly given there are way too many assumptions I do not have good insights on. I also believe building large spreadsheets carries the risk of losing clarity. It can give a false sense of precision. Can’t see the forest, a big tree is blocking my view.

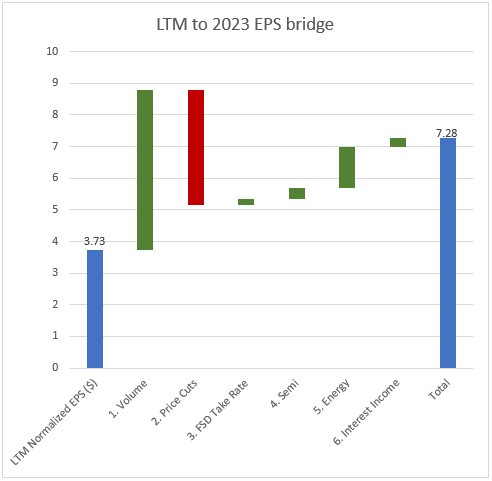

Instead, I will use Tesla’s LTM (last twelve months) performance from 4Q21 to 3Q22 and apply adjustments where I believe 2023 will look different from that. The end result is an EPS bridge at the end of this article, which also includes the underlying Excel workbook for paid subscribers in case you would like to play with the assumptions yourself.

1. Volume Growth

Let’s start with the most obvious difference between LTM and 2023, vehicle deliveries. Tesla delivered 1.2m vehicles LTM. This year they will likely do 2m. In 4Q22, they were already at 1.76m production run rate.

LTM ASP has been $54k per vehicle and Tesla typically incurs $32k in incremental COGS for every additional vehicle they sell. The chart below demonstrates the close and stable relationship between quarterly delivery increases and accompanying increases in COGS. The slope of the regression line can be interpreted as cost for every additional vehicle. All of this relates to the automotive segment only and is adjusted for regulatory credits.

If you have not realized the significance of the chart above: It epitomizes the power of Tesla’s operating leverage. Across the entire income statements, gross profit per car is 15k. But every additional vehicle rakes in 54-32=22k!

Based on this, if they increase deliveries by 800k in 2023 vs. LTM, then the incremental profit is $17.5bn or $5.06 per share.

2. Price Cuts

This is the big elephant in the room. How much will they have to reduce prices to pump this production increase into their end markets? Particularly given overall economic uncertainty and sky-high interest rates making premium vehicles less affordable because they are often leased.

In China, they have already slashed prices by more than 10% and we will have to see how demand will react to it in the coming weeks.

China accounts for ~29% of Tesla’s revenues. What about the remaining 71%?

Most of that is generated in the US. Tesla sells 40% of their vehicles in the US where the government will effectively pay for a 5-15% price cut this year.

The remainder is mostly generated in Europe, where Tesla is currently destroying domestic manufacturers. There seems to be enormous pent-up demand for Teslas in Europe.

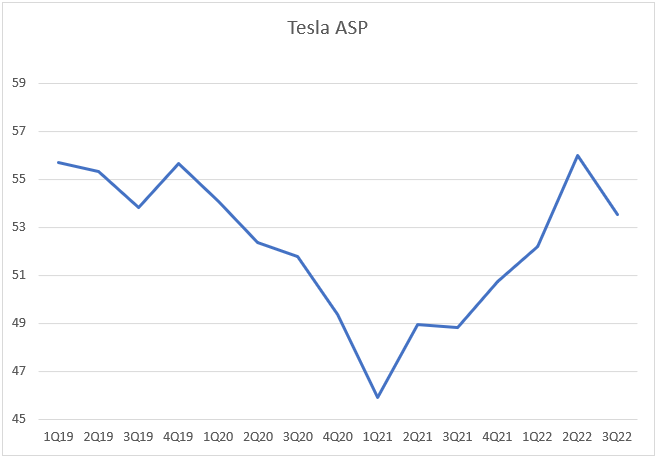

Is there any way to quantify the ASP downside? The chart below shows how it evolved over time. The most notable observation is the 2021/22 spike. While ASPs moved down before due to product mix shifting to higher volume and cheaper models, the last two years have been characterized by an enormous demand wave which had to be crushed by Tesla by raising prices to avoid absurdly long wait times.

We are now in the process of unwinding this. Where will the floor likely be? The dip to 46k in 1Q21 feels like a midterm floor to me. Even if inflation (i.e. the rate of change of the CPI) is now contained, I don’t think the absolute CPI level will go back to pre-spike levels. Also, that was pre-IRA. 46k would be a 15% reduction vs. the LTM average of 54k by the way.

Pierre Ferragu’s tweet below gives great insight into demand elasticity.

Based on their current vehicle line-up, Tesla can access 20% of the US market accounting for ~3m vehicles. If they drop their prices to 46k, they would expand their addressable market to 30% or ~5m vehicles. Auto sales are extremely price elastic because affordability trumps most other purchase considerations. In a sense, the auto market moves based on principles that resemble the housing market.

It seems unlikely to me that we will see more than 10-15% price reduction in the US and Europe in 2023 on average. Price reduction born by Tesla that is. Remember than 5-15% price reduction will be born by the tax payer in the US. So, if Tesla slashes prices in the US by 15%, we are easily talking about a 20-30% effective price reduction. This would unleash enormous demand in my view.

This parameter is highly uncertain of course. But if I had to pick a balanced estimate for 2023 ASP, I would probably go with $48k. If we assume that the ASP will drop from 54k to 48k (11%) for Tesla’s entire 2023 deliveries, this will reduce gross profit by $12.6bn or $3.65 per share when compared to 2m units at $54k in chapter 1.

3. FSD Take Rate

Per the tweet below, Tesla has sold FSD for 285k vehicles so far.

Since they have approximately delivered 3m vehicles so far, the FSD take rate is ~10%. Directionally this is in line with the FSD tracking done by Troy Teslike, a popular Twitter account building bottom up production and delivery estimates.

Their figures are based on self-reporting by readers and therefore likely has an upward bias in the take rate. But it is quite apparent that there was an initial excitement in 2019 (that is when they had their Autonomy Day) about FSD which died down as software progress was slower than expected.

In November 2022, Tesla made FSD available for everyone in North America, not just a small group of selected testers.

I can imagine that this will increase the take rate significantly. People won’t have to buy it anymore hoping about some unknown utility far in the future. They get the utility right away. That tweet from Elon was two thirds into 4Q22. I don’t know how much impact we will see in 4Q22 figure, but I expect the impact in 2023 to be material. Some of the uptake will also be subscription based and therefore not immediately show in revenue. We also don’t know what the take rate was LTM. But we don’t even need to know that. The rate of change is what matters in our bridge.

By and large, I think it is reasonable to assume that 50,000 cars more will buy FSD in 2023 compared to LTM. At a $15,000 price point, this is $750m additional revenue which presumably falls straight to the bottom-line. $0.22 per share.

4. Semi

On Dec 1, 2022, Tesla delivered the first 10 Semis to Pepsi.

The 2022 production target was 100 and the internal goal is to ramp production to 50k units annually in 2024. It is obviously challenging to interpolate between those two figures, but I can imagine that they will do 5k units in 2023.

What do these sell for? Tesla doesn’t reveal that information. The original target price was $180k. I don’t think that comes close for various reasons.

With a 900kWh battery, the Semi would sell for only $200/kWh. This is far below other products. Megapack is at $500, Powerwall at $800, Cars at $700. Not only would Tesla likely lose money making the Semi for this price, it would also take away valuable battery production capacity from profitable products.

There are ENORMOUS subsidies for Semis. Not just the $40k IRA subsidy at the federal level. There are also state level subsidies up to $185k, which would easily put the total subsidy per vehicle way above its original target price. There is huge demand for this vehicle, why would Tesla give it away for free?

nextbigfuture@nextbigfuture[2/8] There are massive state, federal subsidies and subsidies, grants in other countries as well for Electric Semi's. $40k US, $185k NY, $120k CA, Canada, China, EU as well. @SawyerMerrittnextbigfuture.comMassive Electric Semi Truck Subsidies | NextBigFuture.com12:59 AM · Jan 1, 20238 Reposts · 69 Likes

nextbigfuture@nextbigfuture[2/8] There are massive state, federal subsidies and subsidies, grants in other countries as well for Electric Semi's. $40k US, $185k NY, $120k CA, Canada, China, EU as well. @SawyerMerrittnextbigfuture.comMassive Electric Semi Truck Subsidies | NextBigFuture.com12:59 AM · Jan 1, 20238 Reposts · 69 Likes

In my opinion, it will sell for $500k. This would put the price per kWh to ~$550, which I consider reasonable based on production complexity vs. cheaper megapacks and more expensive vehicles.

I estimate that they can build each vehicle for $300/kWh, half of which is presumably battery related. This would yield a gross profit of $250/kWh x 900kWh x 5k units = $1.125bn or $0.33 per share.

5. Energy

There is a new uberbull in Twittertown who models $16bn gross profit from Tesla Energy in 2023, contributing $3.95 to EPS.

For this to be true, Tesla will have to deploy 64GWh in energy storage in 2023 and earn $250/kWh in gross profit (50% margin). They did 5GWh in LTM at a gross profit of 0.

Since 1 megapack comes with 4MWh capacity, they would need to sell 16k units pear year. Per the official Tesla twitter account, their new Lathrop megafactory can make 10k units per year. Lathrop opened late in Q3 by the way. None of it is included in LTM figures.

So, I think it is more prudent to work with an incremental 30GWh (7,500 units to account for uncertainty with ramping), which would lead to $15bn in revenues.

What about margins? I believe there is indeed a strong case for a step change in margins. Megapack prices have increased drastically from $330/kWh to $500-600/kWh, presumably driven by raw material prices. The beauty of megapacks is that raw material price changes flow through to the customers, which is not the case in the vehicles business.

Also, there is near infinite demand for energy storage solutions given the rapid expansion of solar energy and the new IRA subsidies, which gives Tesla strong pricing power. They currently have 50% market share in the US energy storage market.

I can imagine they will earn 30% gross margins on these megapacks which would be consistent with the vehicles business. This would be $4.5bn incremental gross profit or $1.30 per share.

6. Interest Income

From 4Q21 to 3Q22, Tesla had on average $19bn cash and short term investments and their interest and investment income amounted to $165m, implying ~0.9% interest rate.

During that period, the average 1Y US Treasury Yield was 1.7%. It now stands at 4.8%, 3% higher.

As of Sep 30, 2022, Tesla had $21bn in cash and short term investments. In 2023, I believe this figure will be above $25bn on average. Assuming that Tesla will earn 4% on $25bn, this translates to $1bn in interest income, easily $800 more than in the last twelve months or $0.29 per share.

Summary

Summing it all up, my LTM to 2023 EPS bridge suggests that they will earn $7.28 EPS this year:

As a paid subscriber, you can download the underlying Excel file for my calculation below to play with the assumptions yourself if you like.

I believe this to be a balanced and reasonable estimate which reflects Tesla’s macro headwinds, but also gives them credit for all the positive tailwinds.

If Tesla really makes >$7 in EPS this year, the stock will likely appreciate rapidly as this scenario play out. My estimate is ‘only’ 39% ahead of current consensus (so the stock’s typical weekly volatility lol), but I believe investors fear way worse outcomes compared to what is currently modelled by sellside analysts.

Most importantly, $7 EPS would also strengthen the growth story, thereby giving room for multiple expansion. It would also clearly demonstrate that Tesla is a huge IRA beneficiary and a uniquely positioned asset to capitalize on two megatrends, namely energy storage and AI. There is no other company that can be played in both of these verticals. In this scenario, I believe markets would likely assign a 50-60x multiple, which would price the stock at $350-420. I know it sounds insane based on recent price action. But it is the outcome of my analysis in which I tried to be as unbiased as possible (I am however a hopeless fanboy and likely not able to fully comprehend my biases). You can take this as my 12 months price target and remind me of it in one year.

Sincerely,

Your Fallacy Alarm