🔎Are US health insurers defrauding tax payers?

They are gaming the healthcare system, extracting trillions of Dollars from tax payers. Instead of fighting back, people prefer to join the looting of the Treasury by buying health insurance stocks.

TLDR Summary

Medicare Advantage (MA) has become the sweetest honeypot for the entire US healthcare industry. It’s growing faster than overall Medicare spending, which itself is growing faster than overall federal government spending, which is itself growing faster US GDP. Having access to this is like owning a money printer.

MA was established in 1997. It allowed Medicare enrollees to receive their benefits through private insurance companies. The government offloaded some of its insurance function to private carriers with the idea to reduce overall costs by using the power of competition.

This is not working at all. This year alone, tax payers will spend $76bn (!) more for MA enrollees than they would spend for them under traditional Medicare coverage. This is 10% (!) of the primary deficit of the US Treasury.

Over the last twelve years, US tax payers have paid more than $600bn (!) extra to US health insurance companies. The total excess spending since the program’s implementation likely exceeds a trillion Dollars.

This is not a coincidence. Health insurance companies are deliberately gaming the system to get more compensation from the Treasury than a proper risk assessment would justify.

The US Treasury is not treasuring anything anymore. Their doors are wide open for raiders like health insurance carriers. And instead of fighting back, the general public joins the looting by eagerly buying the stocks of these companies. What a cynical world we live in.

Related content from Fallacy Alarm

The original article

On June 24, 2025, I published the article below on UnitedHealth UNH 0.00%↑, America’s largest health insurer.

I argued that much of its business is just freeriding the US healthcare system without provide much value to it. Its most important business segment is Medicare Advantage (MA), which was originally designed to lower costs through the use of private carriers. In theory, these should have an incentive to direct enrollees into a more efficient use of healthcare services, thereby lowering the bill for US tax payers.

However, the average MA enrollee is today far more expensive for the tax payer than he would be under traditional coverage. And why? Because private insurance carriers like UnitedHealth are gaming the system.

Almost a year has passed since I wrote that article. Several reasons make me feel compelled to provide an update:

Firstly, a proper correction has not happened. Instead, UnitedHealth stock is up 33% since then. It has even outperformed the S&P 500 which is up ‘just’ 22% over the same period.

Secondly, the Medicare Payment Advisory Commission (MedPAC) has published their 2026 report in the meantime with updated figures, serving as a reminder that the problem remains unmitigated.

And thirdly, this is not just a story about UnitedHealth. There are several other companies running the same scheme. Their shares prices are also up considerably over the last year, some even more than UnitedHealth.

So, let’s dive one more time into the complex and fascinating US health insurance industry. First, let’s understand how the entire US healthcare system works and how health insurance fits in.

How the US healthcare system works.

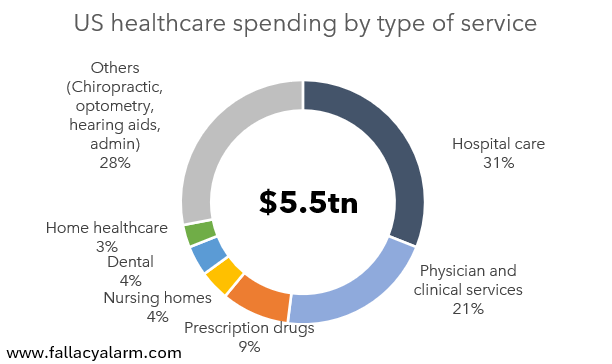

Americans spend about $5.5tn per year on healthcare, which is about 18% of US GDP and about $16,000 per capita. About half of that is spent on hospital care, physician and clinical services. Retail prescription drugs account for roughly 9%, nursing homes and dental services for 4% each and home healthcare for 3%. The remainder includes chiropractic, optometry, hearing aids, other healthcare services and admin services.

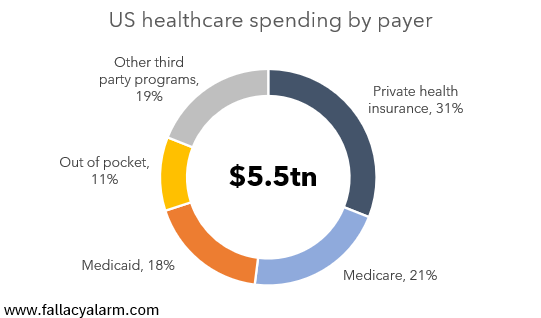

The vast majority of this spending is covered by insurance providers. Private health insurance accounts for 31%. Medicare accounts for 21% and Medicaid accounts for 18%. Only about 11% of healthcare spending happens out of pocket.

This means the payer is not the same as the consumer for about 90% of all healthcare products and services in the US. This separation is a unique feature of the healthcare industry, at least at the scale of trillions of dollars annually. It creates a power imbalance between providers and the economic buyers which the providers can take advantage of.

The issue gets amplified when the economic buyers are not operating for profit and are run by people that have little incentive to keep costs under control. Privately sponsored health insurance plans would shop around if costs get out of control. Public plans are less likely to do so. There are no bonus payments at stake for the civil servants overseeing them.

That’s why Medicaid and Medicare have become the sweetest honeypots in the healthcare industry, esp. for health insurers who have direct access to them. Medicaid offers income-based public health insurance. Medicare offers universal public health insurance for nearly everyone age 65 or older who has sufficient work history.

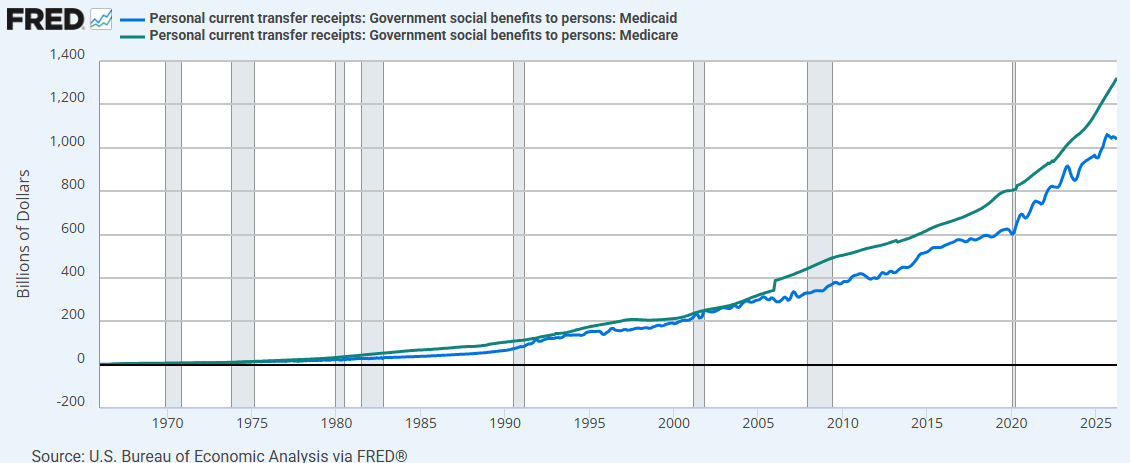

Over the last 30 years, the US Treasury’s spending for Medicaid has grown from $164bn to $1,039bn (+6% p.a.). Over the same period, Medicare spending has grown from $191bn to $1,311bn (+7% p.a.)

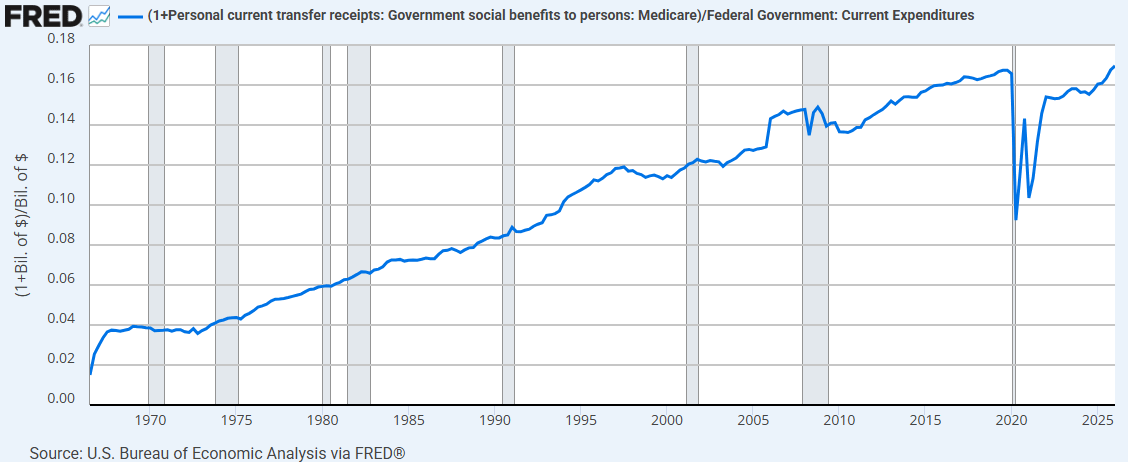

Over the last 30 years, the growth in both cost categories has significantly exceeded average federal expenditure growth which has been 5% on average. Together, Medicaid and Medicare now account for more than 16% of the Treasury’s annual gross spending. Their combined share was 11% in 1996 and less than 3% in 1966.

Some of this is due to demographic reasons. America is ageing and therefore healthcare needs are rising disproportionately. But we have reason to believe that some of this growth is also the result of regulatory failure.

Historically, Medicare operated a so called Fee-for-Service (FFS) model, i.e. the government assumed the role of an insurance carrier. The patient went to a healthcare provider and received a service. Then the provider submitted a claim to Medicare which then paid for each pre-approved service.

In 1997, the federal government introduced MA under which it gave people the option to choose a private insurance carrier. The federal government then paid an annual flat rate for each insured based on a risk score taking various health-related metrics into account (age, sex, existing medical conditions etc.). The goal was to lower spending by letting private carriers manage healthcare services. They were deemed more capable to direct patients into a more efficient use of healthcare services.

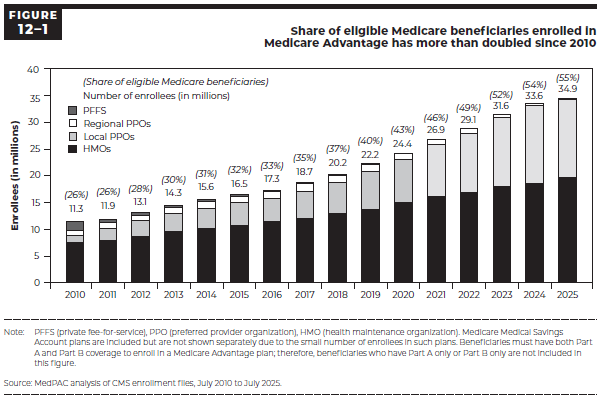

MA has become very popular among America’s seniors. Today, about 55% of all Medicare enrollees are using MA vs. 45% who use FFS.

In 2026, the federal government will pay more than $600bn to private health insurers for administering Medicare Advantage plans. The largest publicly listed ones are UnitedHealth UNH 0.00%↑, Humana HUM 0.00%↑, CVS Health CVS 0.00%↑, Elevance Health ELV 0.00%↑ and Centene CNC 0.00%↑. Their combined MA market share is about 65% and they are sporting a combined market cap of $660bn.

The end game seems to be that MA will be 100% of all Medicare spending. These five companies will keep dominating MA and hence ingest a large share of the entire Medicare spending of the government.

Unless people start reading the MedPAC report which has bombshell information in it…

2026 MedPAC report

The Medicare Payment Advisory Commission (MedPAC) was created as an independent agency by Congress in 1997 to analyze Medicare spending, most importantly with respect to whether providers are paid appropriately.

They published their 2026 report in March 2026. Here’s its key statement:

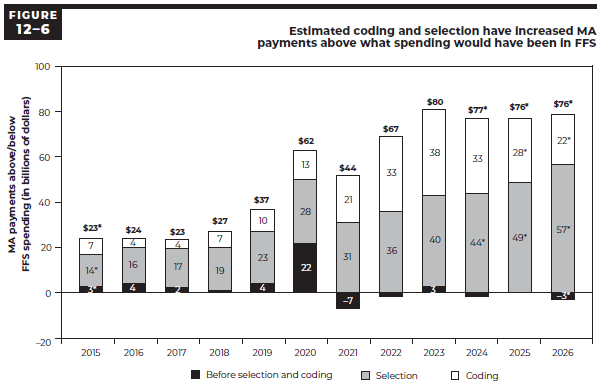

“In 2026, we estimate that Medicare will spend 14 percent—a projected $76 billion—more for MA enrollees than it would spend if those beneficiaries were enrolled in FFS Medicare.”

2026 MedPAC report

It’s a brutal statement which they basically repeat every year with slightly different numbers. Almost thirty years after the implementation of MA, this effectively demonstrates the complete failure of this program. It should make news headlines in my opinion. But it’s being entirely ignored by all media outlets.

Appreciate for a moment how profound this is. The central purpose of MA was to lower costs in the US healthcare system. Instead, it has become a tool for shrewd health insurance managers to extract an enormous amount of money from US tax payers and provide zero value in return.

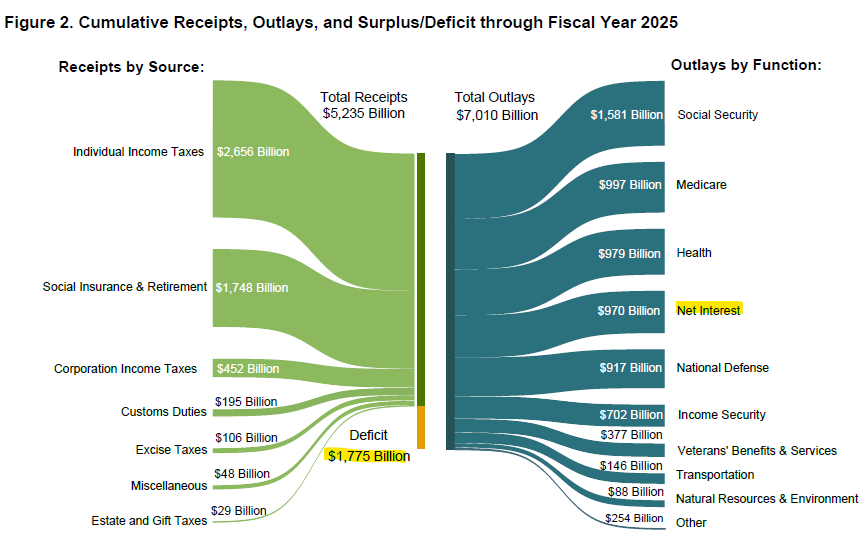

For reference, the US Treasury finished its FY25 with a $1,775bn deficit, $970bn of which was net interest. Hence, its primary deficit was $805bn.

If MA was abolished tomorrow, the US Treasury’s primary deficit was shrink by almost 10% per year instantly. And nobody would be worse off (except the shareholders of health insurance companies and their employees). It might be the single biggest waste item in the entire budget of the US Treasury. It’s a mystery to my why DOGE didn’t identify it as problematic.

And this $76bn waste is just from one year. The 2026 MedPAC report also lists the historical excess spending back to 2015. The total excess spending for 2015 to 2026 amounts to $615bn.

Isn’t it crazy how this information is in the wide open and nobody cares about it?

Now you might be wondering…

How exactly are health insurance carriers gaming the system?

The MedPAC report distinguishes two main types of excess spending both of which result in the measured risk score (and hence compensation to insurers) being too high:

Selection: Select patients who are generally healthier in ways the risk model doesn’t measure.

Coding: Document more diagnoses to get a higher risk score and hence a higher payment.

There are various ways how an insurance carrier can game this. With respect to selection for example, they can design their plans to appeal to seniors who have gym memberships or who are generally active. There are tons of variables with predictive power about someone’s health trajectory that don’t go into the risk scoring.

And once they have these seniors with above average health, they can dial up the payment from the government by encouraging these patients to document more medical conditions even if these conditions won’t immediately raise the likelihood of medical treatments. For example, they can pay for preventative health screenings to uncover abnormal health data, they can educate physicians to improve documentation or they can use software to identify missing diagnoses.

I’m not just speculating here. Most major health insurers have been found or suspected guilty of similar wrongdoing. CVS paid $118m in March 2026 over coding allegations. UnitedHealth is currently under criminal and civil investigation as I discussed in my article last year. Humana and Elevance have faced lawsuits about illegal broker kickbacks for advantageous selection. So far, these remain isolated events without a major public outcry. When caught, companies just pay to keep playing. That’s how the modern US economy works. We have seen it unfold many times in the tech industry for example.

Isn’t this an unacceptable situation? Why is this not a media scandal?

You probably remember Dieselgate. In 2015, Volkswagen was found to have test-rigging software in its cars. The cars knew when they were in an emission testing situation and throttled emissions to comply with emissions regulations. It was a huge scandal. It cost the company $35bn in fines, settlements and compensations. Volkswagen stock dropped 65% in six months. The reputation of the diesel engine collapsed. Numerous executives were prosecuted.

What you may not know is that the underlying information for this scandal had been in the public domain for years before it hit the mainstream. It was an open secret among many engineers and academics. Between 2000 and 2015, numerous third parties tested the real world emissions of Diesel vehicles and noticed that they vastly exceeded the test results. The cheating technology was so well known that it even had a name: defeat device.

I don’t know whether US health insurance companies are merely taking advantage of a system that happens to be rigged in their favor or whether they actually have the criminal energy to manipulate the system at a larger scale in a way like auto OEMs did. Hardly anyone can blame them if they merely apply data analytics to optimize their profits. But what if they are actively bribing policymakers to turn a blind eye on their scheme? $600bn per year is a lot of money and a strong incentive to spend some money on lobby work.

It’s certainly suspicious that the government is not acting on a financial leak of this size. Shouldn’t it be easy to mandate health insurers to disclose their internal risk models to adjust the risk scoring to a more appropriate level? After all, tax payers are paying them hundreds of billions of dollars per year, justifying much of their stock market valuations.

Dieselgate proves that a scandal can take a long time to brew. Evidence of wrongdoing hitting the public domain is not a sufficient condition for it to erupt. The information needs to be spread by the large information multipliers, like media outlets, politicians or influencers. Elon could put this into the spotlight with one tweet. But he’s busy obsessing about other scandals. So, the scheme will continue. For now.

Sincerely,

Rene

Excellent summary of the MEDPAC report. I would look into how rebates work though; it's not quite a flat rate based on risk score.