🔎Aurora Innovation 1Q26: Time to scale.

The commercial launch of robotrucks in America's Sun Belt is possibly the biggest and most underreported story in the world of autonomy right now.

In October 2025, I published the piece below on Aurora Innovation.

I had always been wondering why everyone seems to believe that urban robotaxis should become the first commercial application of autonomous driving. The global freight trucking market is about 10x the size of the global taxi market, cargo freight is much less needy than human freight, and long-distance trucking comes with much less route variation than short-distance ride-hailing which helps manage edge cases.

Aren’t robotrucks much more logical to develop than robotaxis? Aurora’s mission is to figure out the answer to exactly that question. When I published my article, the stock was at about $5 and in a process of trending down. But it has been exploding recently. It’s at $7 now, up 75% from a month ago. Yesterday, they announced 1Q26 results, which is a great opportunity to provide an update.

TLDR Summary

It’s possibly the biggest story in the world of autonomy right now and it’s severely underreported in the media and in the financial community: Aurora is currently commercially launching its virtual railway system on US highways. Management guidance implies that the company could ramp to revenues north of $200m next year with hundreds of trucks in operation.

For reference, Waymo was allegedly at a $350m revenue run rate in December 2025 and raised capital at a $126bn valuation in February 2026. Aurora’s current market cap is ‘just’ $14bn.

This commercial launch validates Aurora’s proprietary LiDAR technology which its competitors will have a hard time to replicate. The company seems to be years ahead of its competition. And that competition is primarily comprised of cash-poor start-ups without much differentiated technology. Most big players have given up on robotrucking. The technological challenges seem too grand.

Management is also guiding for a transformation of Aurora’s business model next year. In the future, their customers will own the trucks and Aurora will manage the driving system, i.e. engaging with all relevant stakeholders from truck OEMs, self-driving hardware manufacturers and software vendors. They could become a capital-light, high margin systems integrator, essential for much of the entire North American robotrucking build-out.

Investment case recap

To fully understand the opportunity, check out the original article linked above, which goes into much more detail than this brief recap.

Long-distance robotrucking is in many ways more exciting for autonomy than urban short-distance ride-hailing. The market is manifold larger. It’s also highly labor intensive. And there is less route variation which reduces the edge case problem.

In spite of its attractiveness, robotrucking is disregarded by most big tech companies and many autonomy start-ups. Tesla hasn’t progressed with its Semi project in years. Waymo mothballed its robotrucking project in 2023. A bunch of other robotrucking start-ups haven’t created much investor excitement so far.

The reason for this lack of excitement is technological: Since 80% of freight trucking is happening on highways, a robotruck must be able to operate at highway speed to be commercially viable. Existing sensor technology can get challenged at that speed. Some sensors may have longer range than others and as a result they might provide conflicting information or critical information that comes to late.

Aurora’s proprietary Frequency Modulated Continuous Wave (FMCW) LiDAR technology is a key differentiator that allows them to operate at higher speeds than traditional Amplitude Modulation (AM) LiDAR systems. Most autonomy developers buy AM LiDAR from external vendors (or famously disregard LiDAR entirely like Tesla). Waymo has its own AM LiDAR technology. Switching to FMCW would be very costly for them. If FMCW works the way Aurora hopes and claims, they would prove to be years ahead of their competition.

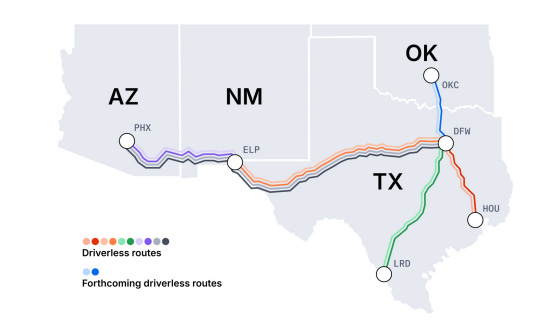

This is the critical context for their commercial launch. The company started to launch their road network in 2Q25 which greatly adds to the credibility of their technology claims. They plan to build a virtual railway system on US highways that will be very flexible in expanding, densifying and changing depending on what customers need and want.

1Q26 earnings

From a pure financial perspective, their earnings release is not yet interesting. They generated just $1m in revenue in 1Q26 and a net loss of $223m which equates to $0.11 per share. For the full year, they are guiding $14-16m revenue, more than 50% of which is expected in 4Q26. Their expected cash burn for the remainder of 2026 is $600m. They have $1.3bn left in the bank. Management believes this is sufficient to bridge them to cash-flow breakeven.

What matters more than the financials at this stage is qualitative commentary and guidance on their roll-out.

Network development

Their network now encompasses 12 distinct routes linking Phoenix, El Paso, Dallas-Fort Worth, Oklahoma City, Houston and Laredo.

They have 7 driverless customers on these routes, including Hirschbach, Uber Freight, Werner, FedEx, Schneider, Detmar and Volvo Autonomous Solutions.

Fleet development

They plan to launch their 2nd generation commercial hardware kit in 2Q26 and the 3rd generation in 2027. Their primary vendors are NVIDIA and Aumovio (a spin-off from German automotive supplier Continental) and Roush (US-based vehicle upfitter).

The company plans to finish 2026 with more than 200 driverless trucks in operation which translates to an annual revenue run rate of $80m. Management commentary further implies that they plan to keep scaling their business far beyond those 200 units in 2027. At such a level, the company would truly have arrived at a commercial stage.

“For the program based on the International® LT® series vehicle, our upfitter, Roush, will begin scaled production later this year. We are initially establishing with Roush the capacity to produce 1,000 trucks per year, with potential to increase that capacity.”

1Q26 shareholder letter

The 2026 guidance implies $400k in annual revenue per truck by the way. For reference, this seems to be a considerable premium to traditionally operated trucking revenue. Owner operators gross about $200k to $350k per year.

Regulatory development

Aurora’s long-term goal is obviously to span their virtual railway system across the entire US. To get there, each state must provide a regulatory framework to enable their operations. Big news came out of California on that front last week. On April 28, 2026, California’s DMV approved new regulations allowing the testing and deployment of autonomous heavy-duty trucks on public roads, removing a long-standing restriction on vehicles over 10,001 pounds. It’s an important step in one of America’s most important states toward commercial autonomous freight operations.

Business model transformation

The company plans to launch their Driver as a Service (DaaS) business next year under which their customers own the fleet in contrast to their current Transportation as a Service (TaaS) business where Aurora owns the fleet. This steps feels logical because it allows Aurora to avoid competing directly with their existing and prospective customers which are trucking companies themselves. It also allows Aurora to focus on its core competency, namely delivering on a reliable full self-driving system, without worrying too much about all other factors impacting the management of a traditional trucking business. If DaaS flies, it could transform Aurora’s operations into a capital-light, high margin systems integrator.

The first customer to test the DaaS offering is Hirschbach, which plans to partner with Aurora to own and operate 500 autonomous trucks. Aurora management frames this deal as an opportunity for “a potential multi-year revenue stream in the hundreds of millions of dollars”. Watch out for more deals like this if you are following the company.

Whether all these ambitions come to fruition as quickly as promised or not, there is in my opinion huge potential here for a powerful narrative, exactly of the kind that markets seem to love these days.

Sincerely,

Rene

I think the major bottleneck for autonomous commercial trucks will be regulatory hurdles. Although these trucks will likely be safer than human drivers in the aggregate stats, the catastrophic consequences of individual accidents will be hard to stomach for many people. When semis crash on the highway around other human drivers there can be numerous deaths and hours of highway shutdowns. These aren't average fender benders. Regulatory agencies could be swayed politically to severely limit autonomous trucking permits, at least within city limits.