🔎goeasy: Ouch! 🤕(incl. Excel workbook)

Rising delinquencies, rising refi costs, mistakes with risk management and accounting, what a mess! But it's actually not as dire upon a second glance. There are several reasons to be bullish.

goeasy will finally report 4Q25 earnings tomorrow after market close. Hence, what I’ve written below may be outdated relatively quickly. I’m basically just giving you 20 hours to read this piece. 😉 I’ve decided to take my chances and publish anyway because I believe there are several interesting points to be raised before we know their earnings. I’m actually quite excited about this setup. Might share an update with you later this week if I have more to say.

TLDR Summary

It’s the perfect storm. First, the company struggled with rising delinquencies and rising refinancing costs. Then they shot themselves in the foot by revealing insufficient risk management and accounting practices. As a result, investors are running for the doors. Reputation destroyed. And rightfully so.

But the situation might actually be less dire than it seems at first glance. The company managed to refinance their debts quickly. A liquidity crunch a la Silicon Valley Bank is off the table. I expect that they will guide 2026 to be profitable when they release earnings tomorrow.

The company’s cash generation is prolific and will recapitalize them rapidly. Not getting a dividend for a while is a small price to pay. Flushing out dividend investors now might in fact help with forward returns.

At 0.5x P/B, markets have priced in that the company’s distribution network is worth nothing and that there are $600m of additional charge offs hidden in the books. I consider that way too punitive.

The original investment case

About two years ago, I published the bullish piece below on goeasy Ltd.

I argued that a global rate cutting cycle was incoming and that this rate cut cycle would perhaps for the first time ever not coincide with a slowdown of corporate earnings, but an acceleration thereof. I further argued that this would cause surging credit demand, especially from borrowers that were hit hardest by the prior tightening cycle.

In my opinion, the case for that scenario was stronger in Canada than in many other places. Monetary policy was ultratight in the context of tight fiscal policy and overleveraged household balance sheets. I felt that goeasy was well-positioned to capitalize on incoming rate cuts.

They had been consistently taking market share from chartered banks, which had been subject to much tighter lending standards since the GFC. Immigration continued to be the main economic growth driver and newcomers tended to have low credit scores which would make them turn to alternative lenders. At that time, the stock was trading at $160.

I updated my view in September 2025. There had indeed been a number of rate cuts between my first and second article. However, the Bank of Canada had been pausing rate cuts for much of 2025. I reckon they feared another inflationary impulse should rate cuts put more pressure on the Canadian Dollar.

Policymakers were stuck between a rock and a hard place. Cut rates to save the real estate industry, the most important industry of the country. Or keep rates high to defend the value of the Dollar and hence the attractiveness of the country for international capital.

At that time, goeasy stock was trading at $210. They had kept growing and printing money in spite of Canada’s dire economic situation with falling real GDP, rising unemployment and weak credit demand. At 12x LTM earnings, I didn’t feel that the stock was overly ambitiously valued given their growth and the potential for Canada to eventually regain some economic momentum. I felt moderately bullish.

The crash

The stock started sliding shortly after my second article. The biggest catalyst were 3Q25 earnings on November 5, 2025 which made the stock drop 20% in one day. They missed consensus by 11% on EPS, primarily due to higher delinquencies. Management blamed the softness of the Canadian economy.

“As we have mentioned previously, the Canadian economy continues to operate under a degree of economic pressure not seen since the COVID pandemic. Unemployment at 7.1% is at its highest level since May 2016, excl. the volatile years of 2020 and 2021. GDP growth is absent, Q2’s number coming in at negative 1.6% annualized. With over 70% of small and medium businesses impacted by tariffs and 18% of Canada’s GDP coming from exports to the US, there remains a high degree of economic uncertainty about the future.”

Jason Appel, Chief Risk Officer, 3Q25 earnings call

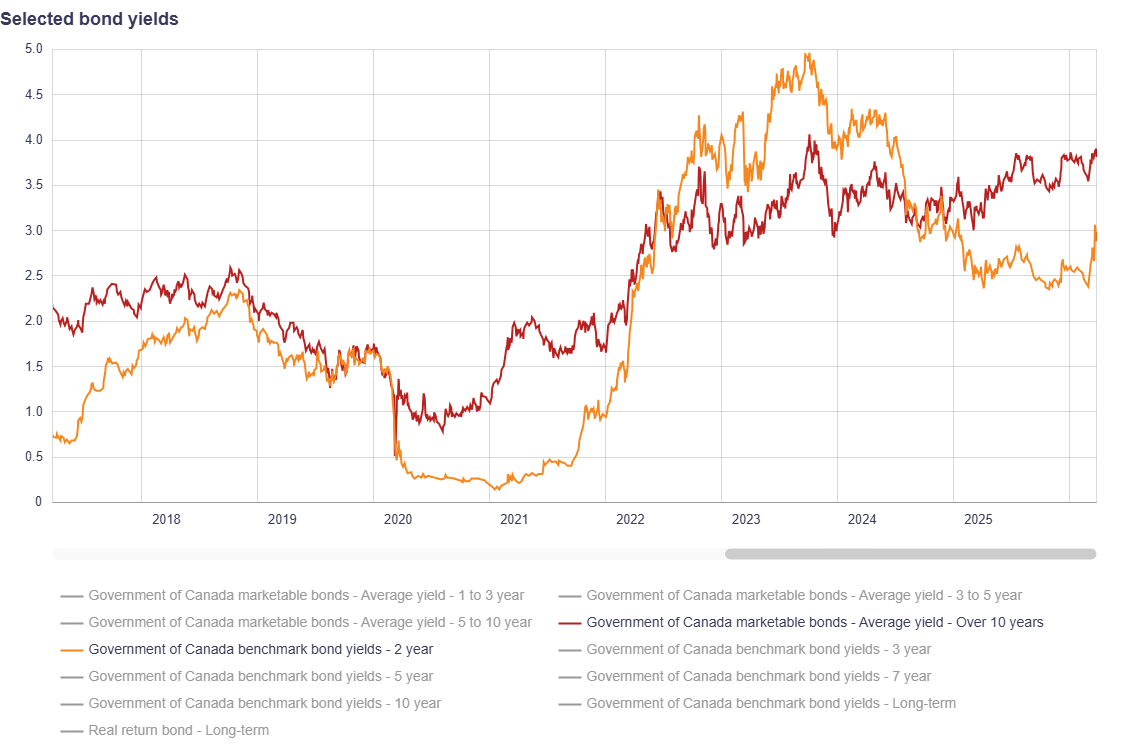

In addition to the economic weakness, interest rates had resumed climbing in 2025. The 2-Year is lately even signaling that rate hikes might be in the cards.

The mix of rising delinquencies and tightening financing conditions was a toxic cocktail for goeasy stock. It finished 2025 at just $131.

This trend continued in 1Q26. By March 9, 2026, the stock had dropped to $110.

Then, on March 10, 2026, the company issued a profit warning. They announced that they expect to incur

an incremental charge off in 4Q25 of $178m against gross consumer loan receivables of $5.5bn and a related write down of $55m for loan interest and fees,

a total net charge off in the quarter of $331m for 4Q25 and

they withdrew their outlook for 4Q25 and their three-year forecast.

The incremental charge off relates to their LendCare segment, a subsidiary that goeasy acquired in 2021. It seems that LendCare grew its loan book too aggressively with insufficient credit risk management practices. They also revealed weak accounting practices. Some interest payments were considered received when they were in fact still being processed. Pretty bad look!

As a result of that write off, the company didn’t comply with certain financial covenants anymore which required refinancing negotiations with their lenders. They postponed their 4Q25 earnings release from March 25 to March 31 to be able to come to an agreement before.

All in all, a pretty terrible picture. The stock is now trading at just $36, down 66% over the last month and 83% from the top. It’s a full-blown crisis of trust, potentially lethal for a leveraged lending business.

However, I do believe there are reasons to be optimistic about the eventual outcome. It’s a high risk/high reward situation. Here’s why some optimism is warranted for tomorrow.