Root 1Q25 earnings preview

What I will be focusing on in my earnings review. What a cross-read from the earnings of Allstate, Progressive and GEICO signals for the company.

Disclaimer: The information contained in this article is not and should not be construed as investment advice. This is my investing journey and I simply share what I do and why I do that for educational and entertainment purposes.

TLDR Summary

When ROOT 0.00%↑ releases their 1Q25 earnings on May 7, I am primarily interested to see to what extent they can confirm the profitability they have achieved in the last quarters. In contrast to most manufacturing or services businesses, financial services are typically much less demand constrained. With enough capital to burn, anyone can build the largest bank or insurance carrier in the world. If you pay depositors 20% per annum or charge $100 for a car insurance policy, you will attracts tons of customers. However, turning that into a profit is a whole other question.

In most businesses, growth precedes profits. In insurance, profitability precedes growth. Capital is the central constraint to growth. And the more profitable the underwriting is, the easier it will be for the insurance carrier to scale up. The more profitability Root will show, the more will investors be willing to price in underwriting growth. This process could become explosive once a capital injection from Carvana’s warrants becomes more probable.

Root’s closest peers Allstate ALL 0.00%↑ , Progressive PGR 0.00%↑ and GEICO reported solid auto insurance results in their 1Q25 releases. Growth in underwriting continued and loss ratios declined further. The insurance industry is still benefiting from cyclical tailwinds that I have discussed before and this bodes well for Root’s earnings release. Based on management commentary, I feel however that the insurance cycle is close to its peak. Insurance carriers are clearly overearning right now which actually makes me want to avoid the them. They might also be more vulnerable to tariffs than other sectors because it will take time to adjust pricing to rising claims costs.

However, I consider my Root investment a long-term commitment that I don’t want to trade in and out. I am convinced that their success story over the last 18 months has both a structural and a cyclical component. Structural because they have perfected their policy pricing and policy acquisition machine. And cyclically because the insurance industry has benefited from inflation in their policy premiums and deflation in their claims. The next 18 months will confirm the split between structural and cyclical.

The insurance cycle

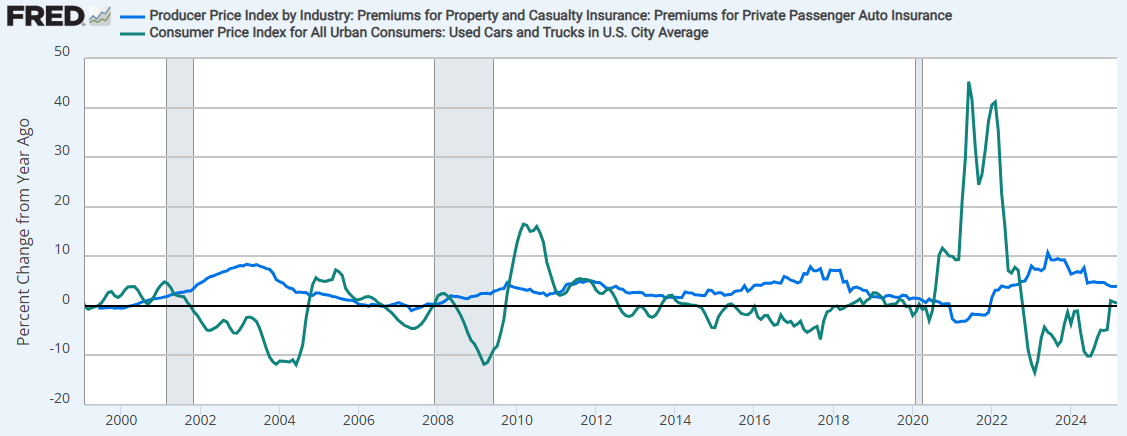

As I highlighted in my 4Q24 earnings coverage, the insurance industry is currently in a cyclical sweet spot because inflation in their premiums is outpacing inflation in their claims.

This inflation delta is mean reverting in nature. In fact, the gap has already started closing. The chart below plots the producer price index for car insurance premiums vs. the consumer price index for used cars and trucks (used as a proxy for claims).

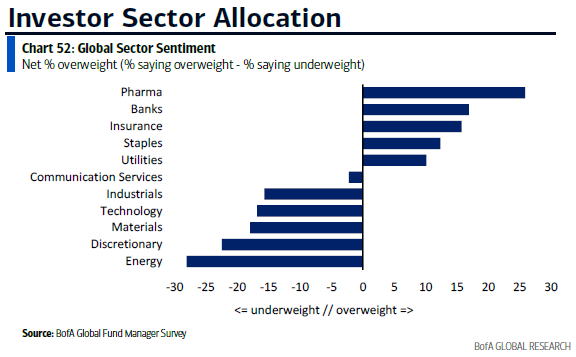

In principle, markets should be able to reflect this cyclical aspect in stock prices. But markets are often not that efficient and this cyclical sweet spot is likely part of the reason why insurance is currently the third most favored sector per the April 2025 Bank of America Global Fund Manager Survey.

High interest rates are playing a role as well because these are beneficial for anyone with interest-bearing (net) assets, which includes banks and insurance companies and also pharma companies that typically have large net cash balances.

Competitors earnings

Allstate