🔎Whirlpool: The best bet on a revival of the housing market?

The stock is trading at less than 3x mid-cycle earnings and the company has a distinct competitive advantage through their domestic manufacturing footprint.

There are about 150 million homes in the US. Combining existing and new home sales, only 4.6 million of these homes got a new owner in the last twelve months. That’s a turnover rate of just 3%. At this rate, the average home gets a new owner only once in almost 33 years.

Homeowners are trapped by ultralow mortgage rates which they don’t want to give up. And potential homebuyers are discouraged by elevated prevailing mortgage rates.

This housing freeze is clearly unsustainable. Irrespective of where mortgage rates are trending, people’s life circumstances change and housing needs do as well. Then they have to move. One way or another, this situation will have to resolve.

There are various ways to bet on such a resolution. One could bet on home builders or mortgage originators. One could buy real estate directly to anticipate a positive price reaction once transaction volume picks up again. Or one could bet on companies making products that people will want to buy when they buy a new home.

Whirlpool is such a case.

TLDR Summary

Break, better or buy. There are three circumstances that make you shop for a new refrigerator: When the old one breaks, when you renovate your home or when you buy a new place. The housing freeze and record low consumer sentiment have effectively removed the latter two of these three occasions.

As the leading producer of major domestic appliances in the US, Whirlpool has been hit hard by this consumer strike. Revenues are down 25% from the pre-pandemic average. EBITDA is down 50%. And the stock is down more than 80% from its peak in 2021.

Virtually all of this collapse is cyclical in nature. There is no sudden increase in competition or substitution. In fact, the trade war strengthens Whirlpool’s competitive position because they manufacture more of their products domestically than their peers.

People need appliances today just like they needed them yesterday. And they will continue to need them even if economic and political disruptions put their incomes under pressure.

Not considering any near-term pent-up demand, Whirlpool should be able to generate $20bn in revenues and $1bn in net income sustainably at a mid-cycle level. This puts the stock’s current price to midcycle earnings multiple at under three.

Related content from Fallacy Alarm

Company background

If you’re from the US or Canada, this company probably doesn’t need introduction. If you’re not: They produce and sell domestic appliances, basically anything electrical you need to run your home, including refrigerators, washers, dryers, dishwashers, ovens etc.

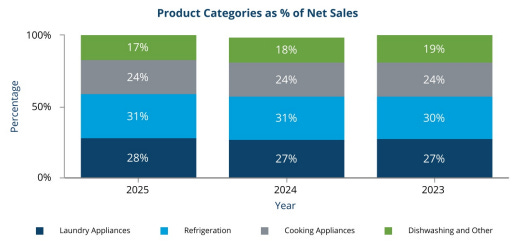

These products are typically categorized as major domestic appliances (MDAs) and account for more than 90% of the company’s revenues (75% of which is from North America and 25% of which is from Latin America). Whirlpool generates about $10bn annual revenues in its North American MDA segment, giving them a 23% market share in a $43bn market.

The company’s product offering comes via eight main brands, which are mostly differentiated by consumer segment, ranging from budget/value-oriented to high-end/premium-oriented.

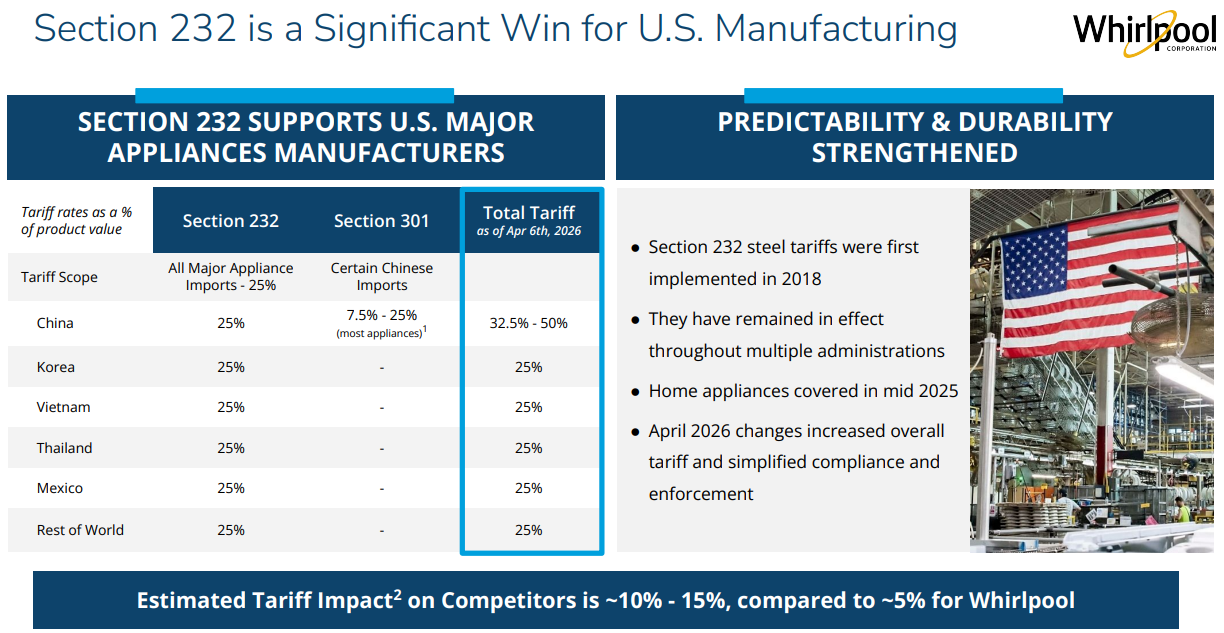

Manufacturing is a key differentiator for the company. 80% of Whirlpool’s MDAs sold in the US are produced in the US and 75% of their SDAs (cooking equipment) sold in the US are produced in the US. They have 11 factories in the US, 6 of which are located in Ohio.

Most of Whirlpool’s competitors are importers and face tariff levies to a greater extent. This is a substantial advantage for the company in the current political climate, where the US administration and the general public want more domestic manufacturing.

“Because we proudly manufacture the vast majority of our products domestically and continue to invest in domestic manufacturing, this trade policy strongly supports our position. We estimate that the 25% tariff impact on our competitors will now be between 10% to 15% of our competitors' total US major appliance net sales. By contrast, the impact of our MDA North America business is estimate to only be about 5%. Ultimately, these changes bring much needed predictability to the industry and deeply strength our competitive advantage as by far the largest domestic appliance producer.”

Juan Carlos Puente, Executive President, 1Q26 earnings call

1Q26 earnings

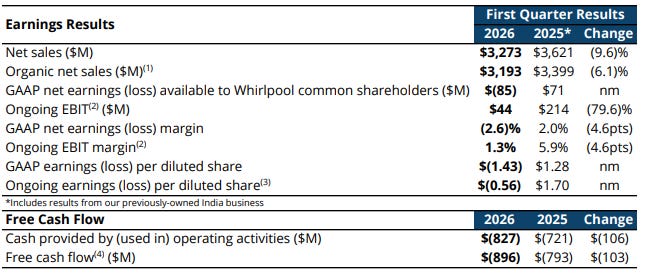

On May 7, 2026, Whirlpool reported 1Q26 earnings. They generated $3.3bn in revenues during the quarter (down 10% YoY, 6% organically) which translated to a modest bottomline loss.

Management primarily blamed poor consumer sentiment for this weak performance:

“The consumer sentiment was already on a very low level by any historical standard. But the war in Iran amplified consumer concerns about the cost of living. As a direct result, the Consumer Sentiment Index in the US plunged, reaching the lowest level on record in March. Now, while our view is that consumer sentiment is unsustainably low and should rebound from here, these events clearly pressured our industry, and particularly discretionary demand. […] The US appliance industry demand declined 7.4% in the first quarter, with March being down 10%. This level of industry decline is similar to what we have observed during the global financial crisis, and even higher than during other recessionary periods.”

Marc Robert Bitzer, CEO, 1Q26 earnings call

They further highlighted that additional downside for the business is likely limited because much of the discretionary demand is absent:

“Keep in mind that we’re operating in an environment where duress replacement demand drives more than 60% of the industry, and this part of the demand is relatively stable. So this gives you a sense about how dramatic the impact on discretionary demand was.”

Marc Robert Bitzer, CEO, 1Q26 earnings call

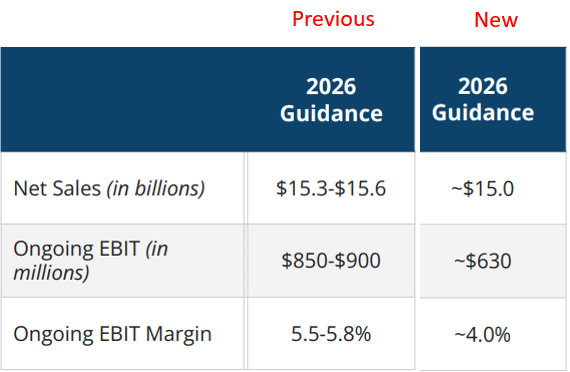

While they don’t anticipate a further collapse of revenue and earnings, they also don’t expect a quick recovery. Therefore, as a response to the operating weakness, management decided to suspend their common dividend to prioritize debt paydown. They also cut their 2026 guidance significantly to $15bn revenues (-3% vs. prior guidance) and $630m ongoing EBIT (-28%).

The stock got diarrhea trying to digest all of that. It’s down another 26% since the earnings release. Today alone it fell another 6% to sub $40 as of this writing.

It feels like a capitulation is happening here. How interesting is this from a valuation perspective?

Valuation

After the recent sell-off, Whirlpool is now trading at a $2.5bn market cap and an $8.5bn Enterprise Value. This means Whirlpool now trades at 0.6x their current year revenue guidance and 13.5x their ongoing EBIT guidance. Looking at its historical valuation multiples, it’s not necessarily cheap based on this year’s performance. But this year is hardly a useful predictor for the company’s long-term earnings potential.

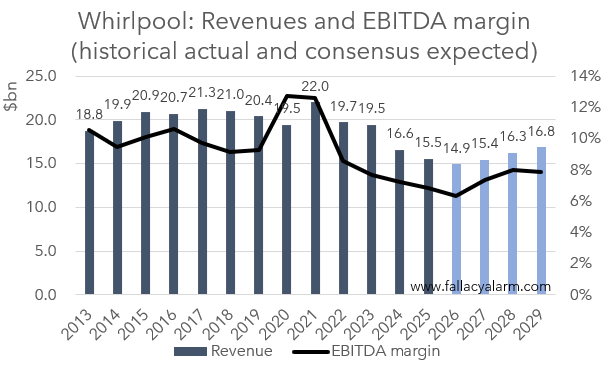

For most of the 2010s, Whirlpool had a fairly stable business with revenues growing modestly, reaching just over $20bn in 2019, and an EBITDA margin hovering at about 10%. The pandemic housing boom gave them a temporary revenue and earnings boost when they generated $22bn in revenues and a 13% EBITDA margin.

Analysts expect that 2026 will be the bottom for Whirlpool’s operating performance. But they are very cautious regarding the subsequent recovery path, not expecting a return to prepandemic levels anytime soon.

I think we can be a bit more optimistic than that, can’t we? Whirlpool’s business is not hit with a sudden increase in competition or substitution. Most of this is a cyclical demand shortfall. And with every day that passes, the appliances installed in American kitchens are ageing another day.

If we assume that the company can return to $20bn annual revenues and apply a 10% EBITDA margin, their sustainable EBITDA is about $2bn. They have about $350m in annual depreciation and amortization which is presumably fairly close to their sustainable capex level. That suggests a sustainable EBIT of $1.65m. Assuming $300m in net interest expense and a 20% tax rates, a high level estimate of the sustainable net income amounts to about $1bn.

That’s only 2.5x the company’s current market cap! And it doesn’t even consider that several years of housing freeze have likely created a sizable pent-up demand. It also doesn’t assume any appliance inflation compared to 2019.

Sincerely,

Rene